Two major reports in the last week have painted a stark picture of the future of the US housing market. Last week’s report from the Urban Institute predicted that the decline in homeownership over the past seven years will be “the new normal.” Then, on June 24, Harvard’s Joint Center on Housing Studies released its own report, “The State of the Nation’s Housing 2015,” echoing many of the same themes.

The bottom line: the single family homeownership market is not coming back for the foreseeable future. And the reasons are as much about demographics as economics.

RENTING UP; OWNING, NOT SO MUCH. As we’ve noted at City Observatory, the shift to renting has been strong over the last several years: since 2007, the number of rental households in the US has increased by 17 million, while the number of owner occupied homes has declined.

The two studies agree that this shift to renting will continue for the foreseeable future. According to the Urban Institute, 13 million of the 22 million net new households formed between 2010 and 2030 will be renters. For its part, the Joint Center for Housing Studies predicts that a majority of those under 30 today will form rental households during the decade ahead.

This trend toward rental housing has become well-established in the past few years. According to the Harvard report, The overall homeownership rate has fallen from a peak of 69% during the housing bubble, to 64% in 2014. The decline since 2007 has erased all of the gains in homeownership of the past two decades, and the national homeownership rate is now down to the same level it was in the early 1990s. (So much, apparently for the much ballyhooed efforts to create an ownership society through housing).

As the Joint Center on Housing Studies (JCHS) report makes clear, there are lots of economic reasons for these trends. Most importantly, real inflation-adjusted household incomes are below the levels they were in the 1990s. Households with less income can afford less housing, and as a result are less likely to be homeowners. Also, today’s young adults are much more likely to be burdened by student debt: The JCHS reports that 41% of 25-34 year old renters have student debt, up from 30% a decade ago, and that debt averages more than $30,000 – up 50 percent from a decade earlier. Finally – and for very good reasons – lending standards are much tougher today, and households with weak credit can’t qualify for home loans as easily as they could in the era of NINJA (no income, no job or assets) lending during the housing bubble. But the growth in renting isn’t just a story of relatively impoverished millennials: JCHS shows that renting levels are up for those 45 to 64, and that households in the top half of the income distribution – which are far more likely to own – accounted for 43% of the growth in the rental housing occupancy.

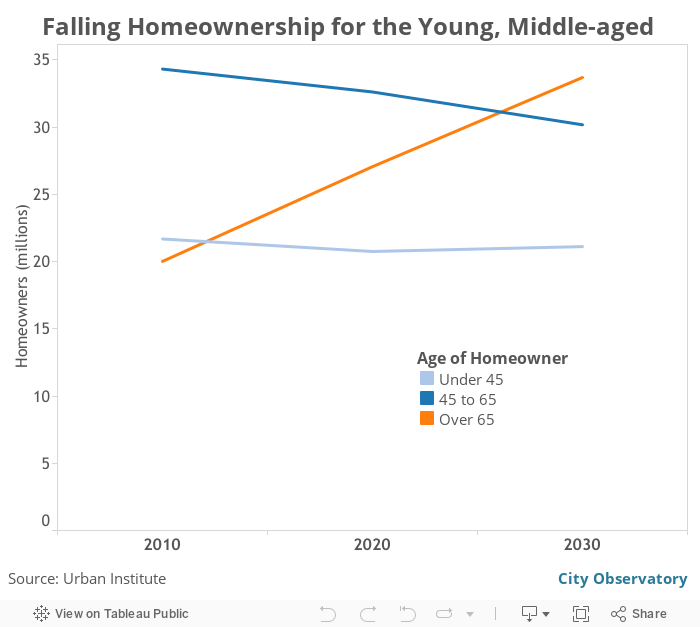

THE “GERONTIFICATION” OF HOMEOWNERSHIP. The other major implication of these two studies hasn’t gotten much attention. The aggregate statistics conceal deeper changes in the pattern of homeownership by age. Over the next two decades, the typical homeowner will be older than today – much older, because all of the net growth in homeownership will be among households whose head is 65 years or older – and the number of homeowners under 45 will decline. The Urban Institute’s estimates are that by 2030, this will produce a pronounced “generation gap” in housing tenure: 34 million homes owned by those over 65 (up from 15 million in 1990) and just 22 million homes owned by those under 45 (down from 24 million in 1990).

Much of the gain in home ownership during the 1990s and early 2000s was the product of demographic forces – the Baby Boom generation maturing fully into its maximum home-owning years. As the JCHS data show, the only age cohort that has higher home ownership today than 20 years ago is those 65 and over. For all age groups under 65, homeownership rates are 3 to 5 percentage points lower today than they were in the early 1990s.

The Urban Institute predicts that the trend toward older homeowners will continue through 2030. All of the net increase in homeownership from 2010 through 2030 will be in households aged 65 and over. The net increase will be about 9 million more homeowners between 2010 and 2030. Homeowning households aged 65+ will increase by 13.6 million rover those two decades. The number of homeowners aged 45 and under will decline by almost a million between 2010 and 2020, and rebound only about 360,000 over the following decade. Thus there will be no NET increase in homeownership by young homeowners over the two decades 2010-2030.

The trends in homeownership are heavily driven by the aging of the US population. Nearly all of the growth in households between 2010 and 2030 will come in households headed by seniors, according to the JCHS projections. Households headed by those under 45 will increase by about 5 million through 2030; households with heads aged 45 to 64 will be nearly flat; and the number of households headed by those 65 and older will increase by about 21 million (JCHS, Table 6).

Rather than gentrification, maybe we need to be thinking about “gerontrification.” The shift in the age profile of the typical homeowner and the growing generation gap between renters and owners is likely to pose big challenges to housing policy.

Will older homeowners want to age in place? Will we experience a housing size and tenure mismatch, with smaller and older households owning homes and larger and younger households primarily renting? These two studies just scratch the surface of these important questions. Stay tuned: these are interesting times for the housing market.