New data shows the diffusion of ride-sharing among US metro areas: Parking prices matter.

We know from casual observation and the occasional leaded corporate document that ridesharing (which is more accurately but clumsily labeled ‘transportation network companies’) is growing rapidly. Although Uber and Lyft are pretty stingy with their data, our friends at the Brookings Institution, Ian Hathaway and Mark Muro, have come up with a clever, indirect way to measure the growth of ridesharing across US metro areas. Because driver’s are, at least on paper, independent businesses, the transportation network companies are required to provide them with 1099 forms listing their income, and in turn, each driver is required to report this income on her or his personal income tax returns. The Census Bureau taps an anonymized version of this tax data to compute the number of self-employed persons reporting business income, as part of their “non-employer” data series. Hathaway and Muro have gathered this data by metro area, focusing in on persons who reported income from being transportation service providers. The net result is a useful index of the scale and growth of the ridesharing industry.

Last week, they released their analysis based on the latest (tax year 2015) data. The key finding is that rideshare related non-employment grew dramatically over the previous year. More than 500,0000 people reported income as transportation service providers, up by 63 percent from 2014. The Brookings report shows in detail the acceleration of growth by metro area.

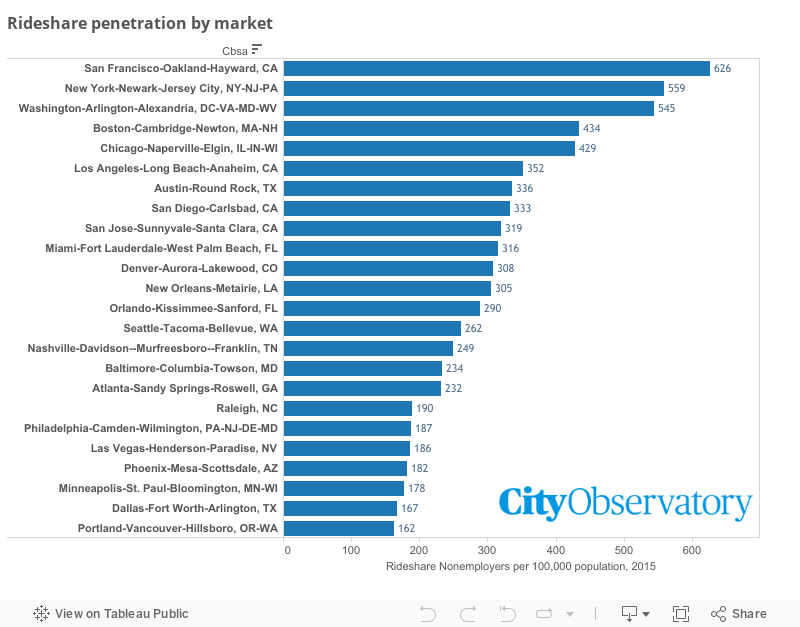

At City Observatory, we’ve been keenly interested in which cities ridesharing is most prevalent, and understanding what characteristics of these cities seem to drive the industry’s growth. We’ve used the Brookings data to compute the relative scale of ridesharing in each metro area by dividing the number of ridesharing non-employers in a metro area by the region’s population. The following chart shows the number of rideshare non-employers per 100,000 population.

Ridesharing is most advanced in the nation’s largest, densest and most tech-oriented cities. San Francisco, New York, and Washington top the list with more than 500 rideshare non-employers per 100,000 population. The median large metro area on our list has about 140 ride-share non-employers. Ridesharing is much less common in the smallest of these metro areas: Birmingham, Rochester and Memphis.

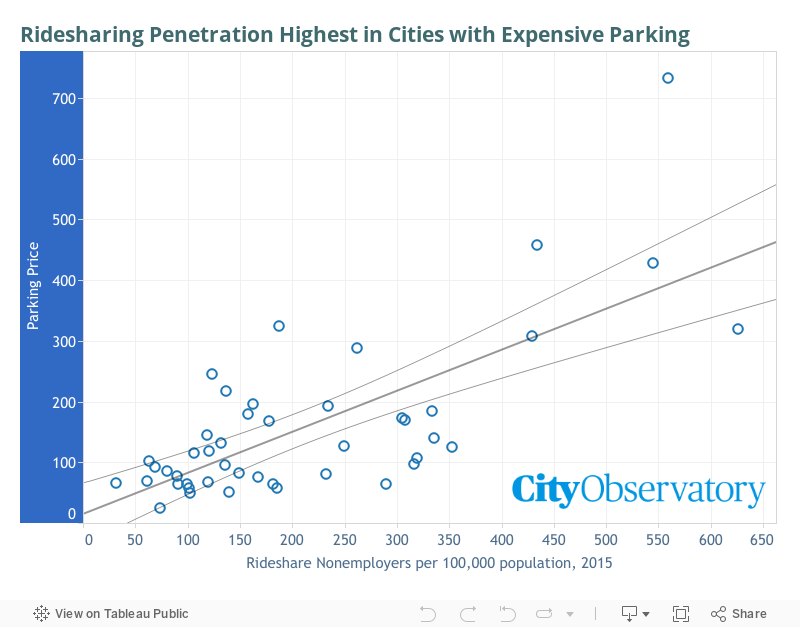

The relative attractiveness of ridesharing hinges on the cost and convenience of alternatives, most notably private car ownership. Uber and Lyft and their competitors provide on-demand service that frees customers from the need to travel to and from where their car is parked, and to have to pay for parking. In places where parking is abundant and free (or at least, un-priced) to car travelers, Uber and Lyft are relatively less attractive alternatives. To these this relationship, we’ve again combined data on the variation in parking prices among US cities (which we calculated by looking up the cost of monthly parking at off-street private lots near each large city’s City Hall), and the Brookings data on the penetration of ride sharing. The data show that the penetration of ride sharing services tends to be higher in cities with more expensive parking.

These data show a similar pattern to the analysis we undertook with 2014 data. The explanatory power of parking price variations declined somewhat (the coefficient of determination was .68 for the 2014 data and .51 for the 2015 data), which suggests that other factors played a larger roll in 2015. This is consistent with a “technology diffusion” model of ridesharing growth: the industry starts and grows disproportionately faster in the cities with the most favorable market conditions (i.e. high parking prices), but then gradually diffuses to other markets where market conditions are less favorable.

The one glaring limitation of the non-employer data is that they come with a significant time lag. We’re only now just learning about the growth of the industry in 2015, and it will be May or June of 2018 before we see then 2016 Census non-employer numbers. It’s also the case that these data are capturing growth in a period of time in which Uber, in particular, has been heavily subsidizing fares. Whether its business model and its growth trajectory are sustainable, is still open to question.

The key takeaway here is that pricing matters. Places that price private automobile operation (even just indirectly through parking charges) prompt travelers to adopt alternative means of transportation. As we and others have noted, the fact that ridesharing services don’t have to pay for access to the street network in peak hours (even though they charge peak prices at these times), leads to more vehicular congestion. As ridesharing grows, and with the advent of autonomous vehicles seeming ever more likely, re-thinking the way we price access to roads will be central to sustainable transportation in cities.

____

Thanks to Ian Hathaway and Mark Muro for sharing the data used in their analysis.