Yesterday, we wrote about the Chelsea neighborhood in Manhattan, which is in the unique position of being one of the wealthiest urban communities in the nation, and also having almost a third of its housing be public or otherwise subsidized. The question was, what happens to the residents of public housing in a place like Chelsea when it gentrifies?

The answer was mixed, but mostly positive. A study from the well-respected Furman Institute at NYU showed that residents of public housing in wealthy or “increasing income” neighborhoods earned substantially more, on average, than public housing residents in low-income neighborhoods. Moreover, they experienced less violent crime and their children went to better public schools—and, likely as a result, did better in school themselves. While low income residents of gentrifying neighborhoods cited problems finding affordable local retail and a sense of alienation from the businesses and institutions catering to their very different neighbors, on balance, many thought their neighborhoods had changed for the better.

But New York City is unique in having such huge concentrations of public and subsidized housing in many affluent or “increasing income” neighborhoods. In most places, low-income residents in low-income communities live in market rate housing that’s affordable because there is so little demand for it from middle class and upper-income households. In those cases, you would expect that as demand increases, those residents would be priced out, excluding them from the benefits of an increasingly resource-rich community.

A new study from the Federal Reserve Bank of Philadelphia challenges this narrative. The authors (Lei Ding and Eileen Divringi of the Fed, and Jackelyn Hwang of Princeton, who has written other notable studies on gentrification) tracked movement in and out of urban neighborhoods in Philadelphia from 2002 to 2014, and look at the effect of rising rents and incomes on existing residents. From our perspective, there are three big takeaways.

First, demographic change in gentrifying neighborhoods doesn’t happen the way most people think it does. Ding et al find that in gentrifying neighborhoods, existing residents are just 0.4 percentage points more likely to move out in a given year than they would be in a non-gentrifying neighborhood. (As a baseline, just over 10 percent of all residents moved in a given year.) Even in those neighborhoods with the most rapid increases in rents and income, existing residents are just 3.6 percentage points more likely to move. Moreover, because the authors are interested in involuntary displacement, presumably for economic reasons, they look at whether people who leave gentrifying neighborhoods are more likely to move to poorer communities. In most cases, the answer seems to be no.

So what explains the changing income and ethnic backgrounds of residents in these communities? In short, it’s not who’s moving out; it’s who’s moving in. People who would have left anyway are replaced by a whiter, more affluent group of people; most neighborhoods have turnover rates high enough that this dynamic alone can change the makeup of a neighborhood’s residents quite quickly. To quote the study: “Overall, the results are more consistent with the notion that changes in the characteristics of inmovers are a more important force in determining the demographic changes in gentrifying neighborhoods.”

Second, the Philadelphia Fed joins the Furman Center in finding that those residents who remain in gentrifying communities see some economic gain. In this case, the authors measure financial health through credit scores. Remaining in a gentrifying neighborhood is worth, on average, a gain of 11 credit score points over three years, compared to a situation in which the resident’s neighborhood did not see rising income and rent levels. It’s not entirely clear why this happens, but rising income (as suggested in the Furman report), or improved access to credit, might be a part of it. Complicating those results, residents with particularly bad credit saw relatively larger increases in their scores, though living in a gentrifying neighborhood was associated with slightly smaller increases than if they had lived in a nongentrifying area.

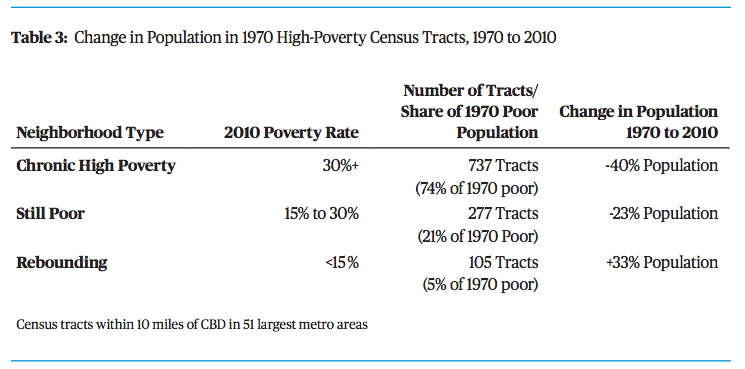

Finally, while many narratives about gentrification suggest that the choice is between neighborhood change versus stability, that is not what the Fed study depicts. While the average gentrifying neighborhood in Philadelphia saw its median income increase by nearly 42 percent between 2000 and 2013, nongentrifying neighborhoods did not remain the same—their median income fell by almost 20 percent, with an almost five percentage point increase in the poverty rate. Moreover, while gentrifying neighborhoods’ population grew by an average of 2.3 percent, nongentrifying neighborhoods lost nearly two percent of their population, driven not only by an exodus of non-Hispanic whites, but also a decline of almost five percent in the population of non-Hispanic blacks. Perhaps most amazingly, the proportion of residents who were housing-cost-burdened increased by over 10 percentage points in neighborhoods that didn’t gentrify—probably because of falling incomes.

We should pause for a moment to note that while the Philadelphia Fed study is valuable, in part because it uses a more detailed data set, none of its results are really new. As Lei et al acknowledge, studies of gentrifying neighborhoods (most famously Lance Freeman’s) have generally failed to find higher rates of outmoving among existing residents, compared to otherwise similar nongentrifying neighborhoods. The finding that residents who stay in gentrifying neighborhoods see some economic benefits, as we’ve already pointed out, echoes what the Furman Center reported in its study of public housing residents in New York, and a Cleveland Fed study from 2013. And the fact that low-income neighborhoods that don’t gentrify also don’t remain the same—that the alternative to a lack of reinvestment is a persistent pattern of economic and demographic decline—is what we found in our own study, “Lost in Place.”

The point here is not that everything in gentrifying neighborhoods is peachy. After all, there’s very little displacement of economically vulnerable people in exclusionary high-income neighborhoods, because there are no economically vulnerable people to begin with. But when there are problems, they’re less likely to be existing residents forced out by rising rents, and more likely to be potential residents who are turned away before they even arrive. The challenge, in neighborhoods that are becoming more affluent as well as ones that already are, is to make sure that there is a sufficient stock of affordable housing (both subsidized and “naturally occurring” at market rate) to accommodate people of whatever means who want to move in. The best way to do that remains to make sure there isn’t an overall shortage of housing, and that there’s a variety of housing types, from single family homes to apartments of various sizes; and to remain friendly to developers of subsidized housing and people holding housing vouchers.

But the fact that rigorous studies of neighborhood change consistently produce results that, at least, complicate widely repeated narratives about gentrification ought to give us pause. While there are certainly people who are forced out of their homes by rising rents, it’s curious that the focus on those cases tends to crowd out attention on people who would like to move to a neighborhood but can’t afford it, a situation that appears to be more widespread. Similarly, the implicit assumption of most gentrification coverage—that the absence of gentrification would result in the preservation of the existing neighborhood as is—clearly needs to be reassessed. We’ll write more about this media issue tomorrow.