There’s a revolution afoot in transportation. Transportation network companies, aka “ridesharing” firms, like Uber and Lyft are disrupting both the markets for urban transportation and labor markets. Their business model–treating drivers as independent contractors, is fueling the so-called “gig economy.” A new report from the Brookings Institution uses federal tax and administrative records to plot the growth in the number of these independent gig workers in the “rides” and “rooms” sectors (think Uber, Lyft and AirBnB). Their report provides a useful new metric from understanding the growth and impact of these sectors. While that’s well worth a read in its own right, the Brookings data also provides a detailed set of metropolitan level statistics that help us judge the places where ridesharing has scaled up the most rapidly.

Released today by the Brookings Institution, this report – Tracking the Gig Economy: New Numbers — estimates the size and growth rate independent employees in two key segments of the gig economy. Mark Muro and Ian Hathaway have exploited a little-used Census data series on “non-employer firms” to look at the growth of independent contracting in the transportation and accommodations industries. (See below for the geeky details of this data source).

The Brookings estimates cover the years through 2014, and give us a pretty good picture of the rate of increase in the number of people reporting taxable income from a non-employing business operation in passenger transportation and accommodations. Their estimates suggest that the employment in ride-sharing increased by about 69 percent between 2010 and 2014. (Data for room-sharing, less well captured due to the nature of tax treatment of rental income, show a smaller, but still substantial increase of 17 percent).

In their analysis, Muro and Hathaway also look at the relative size of the “gig” portion of the accommodations and transportation sectors in each of the 50 largest metropolitan areas compared to the number of wage and salary workers the same industries in those areas. They examine the trend data to see whether the growth of gig workers, say in ridesharing, is cutting into the number of people employed in the taxi business. So far, at least, the results are inconclusive—but another year or two of data may present a different picture, as all indications are that the industry has grown very rapidly in 2015 and 2016.

The Geography of Ridesharing Industry

While much of the Brookings report is focused on the growth of these two key sectors of the gig economy, at City Observatory, we’re always interested in which metropolitan areas are leading the way in the adoption of new ideas. So we set about using the Brookings data to assess the relative size of the ridesharing component of the gig economy in each of the nation’s 50 largest metropolitan areas.

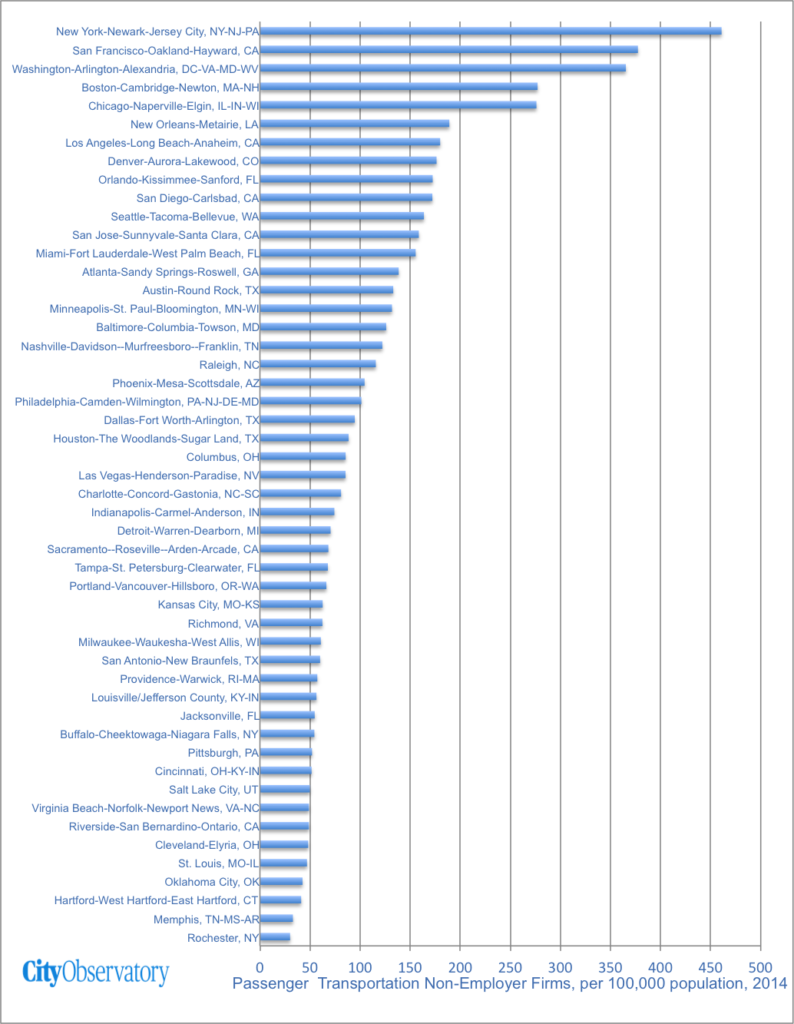

We want to know which cities have, proportionately, the largest concentrations of independent contractors involved in providing passenger ground transportation services. To answer this question, we computed the number of non-employers in this category per 100,000 metropolitan area residents. The typical (median) large metropolitan area had about 83 ride sharing drivers per 100,000 population in 2014. Of course, this number varied substantially among different metros.

New York (461 per 100,000), San Francisco (377) and Washington (365) had the highest concentration of transportation non-employers, with about four to five times as many on a population-adjusted basis as the typical city. At the other end of the spectrum, Rochester, Memphis, Hartford and Oklahoma City had the smallest concentrations of transportation non-employers, with fewer than 50 transportation non-employers per 100,000 population.

It’s apparent that the growth of ridesharing has proceeded most rapidly in larger, denser cities, and has lagged in smaller and more sprawling ones. The richest markets for transportation network companies are where there are lots of potential customers, and where private car travel is expensive and inconvenient. In a future post, we’ll take a closer look at the relationship between metro area characteristics and the penetration of ridesharing, as indicated by the Brookings tabulation of transportation non-employer data.

Cross-checking the data

Because this is such a new and poorly measured sector of the economy, we want to be careful in leaning to heavily on any single source of data. Its worth asking how well the Brookings estimates square with other available data the size and growth of the gig economy. While none of these firms has yet gone public and though they carefully guard many of their financial results, there are a few fragments of data in the public realm. While its difficult to directly compare administrative records and the scanty firm level data, the picture painted in the Brookings report fits well with what we know about the size and growth of Uber in the transportation networking market.

In late 2015, Uber reported that it had more than 327,000 active drivers on the road in the US, a figure more than double the 160,000 on the road in 2014. (Active drivers were those who had provided more than four rides in a month. The Brookings report estimates that in 2014, there were about 341,000 non-employer firms engaged in taxi, limousine and ground transportation services, up about 112,000 from two years earlier. Allowing for the fact that many drivers may have worked only part year, or too few hours to be counted by the Census Bureau, that seems like a roughly consistent pattern of growth.

Business Insider reports that Uber had about 5,600 active drivers in San Francisco at the end of 2013. Brookings reports that there were about 7,000 non-employers in the transportation services categories in 2012 and about 17,000 in 2014. This suggests that Uber’s active drivers were equal to about half of the reported number of non-employers (assuming steady growth between 2012 and 2014).

Geeky data details

The most commonly reported data series for the economy report non-farm wage and salary employment—the number of people on the payroll of governments and private businesses. Using administrative records—tax returns filed with the Internal Revenue Service—the Census Bureau computes data on people working for themselves. Most of these firms are in the so-called “1099 economy” – people who instead of receiving a W-2 from an employer receive a form 1099 indicating that they’ve received a payment from a firm but that they are not an employee of that firm. The 1099 form also picks up income from investments–like rents and royalties–and some non-Internet businesses would clearly be captured by this same data source (say an independent, sole-proprietor taxi driver, or someone who ran an actual bed-and-breakfast). But the growth in this category in the past few years is likely to be very indicative of the growth of these businesses.

The Census Bureau tabulates these records according to industry (using the North American Industry Classification System – NAICS) and by county. Muro and Hathaway aggregated the county level data up to metropolitan areas, and looked at the statistics for two particular sets of NAICS codes (roughly corresponding to taxi and limousine services and other ground transportation providers, and rooming houses and other accommodation.