It’s been debunked, right? Though we’ve long been told that millennials want to live in cities, renting rather than owning, and biking instead of driving, a new round of articles are here to tell us that all of that is a myth: as soon as they find their financial footing, young people are buying homes in the suburbs just like previous generations.

These latest claims about housing are based on a new National Association of Realtors study. Based on its annual surveys of recent homebuyers, the NAR reports that millennials now make up 35 percent of those who had purchased homes in the past year, up from 32 percent in 2014, and 31 percent in 2013.

But, if you’ll forgive the paraphrase, these numbers—they do not mean what the NAR thinks they mean.

The basic problem is that the NAR—and other, similar reports (for example, about car-buying habits)—are confusing lifecycle effects with generational effects. Lifecycle effects describe how people’s behavior changes predictably as they get older. A generational effect describes how a cohort of people born at a certain time are different from another cohort of people born at a different time: so, for example, how a millennial behaves at age 25, compared to how previous generations—gen x-ers or boomers—behaved at age 25.

Life Cycle vs. Generational Effects

So when the NAR reports that millennials are buying more homes as they get older, we have to ask if this is a lifecycle effect or a generational one. After all, even if millennials are less likely to buy homes compared to earlier generations, it would be very strange if millennials bucked the well-established lifecycle effect of being more likely to buy a home in their 30s compared to their 20s.

The NAR statistics about market share can’t answer this question, because they compare the home buying habits of 18- to 33-year-olds in 2013 with 20- to 35-year-olds in 2015. For market share to remain the same across these samples, the 34- and 35-year-olds added in 2015 would probably have to buy homes at the same rates as the 18- and 19-year-olds who were dropped. But people in their mid-30s have always bought more homes than people just out of high school, and that lifecycle effect doesn’t signal any shift away from the underlying generational decline in homebuying.

In effect, all the NAR has proven is that, when they are older, millennials buy more homes than when they were younger. But as we’ll show below, at any given age, millennials are still less likely to be homeowners than previous generations at the same age.

Comparing Millennials to Previous Generations

To check for generational change, you have to compare identical age cohorts over time. And if you do that, it’s clear that millennials are, in fact, less likely to buy a home than earlier generations. Homeownership for every cohort under age 65 is depressed well below historic levels, especially for people now in their thirties, and this decline continuing, not reversing.

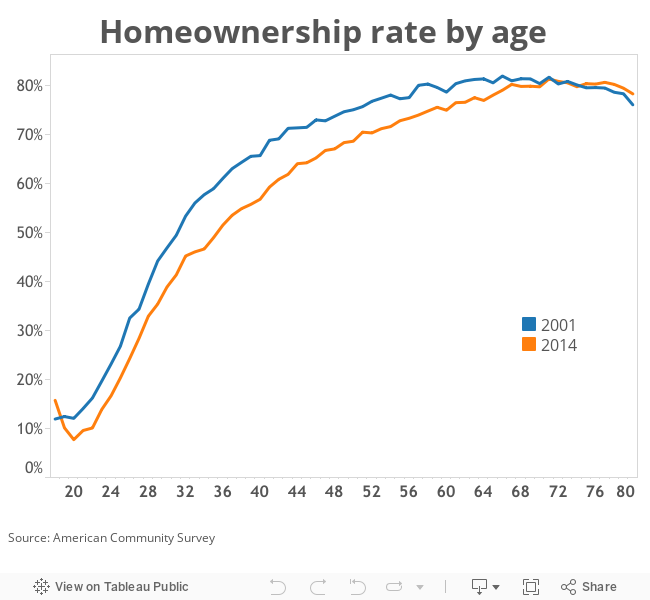

This chart shows how homeownership rates have varied by age for two years: 2001 and 2014. You can see that in both years, homeownership rates increase steeply in the for persons in their late 20s and early 30s, and then grow more slowly as people age into their 50s or 60s.

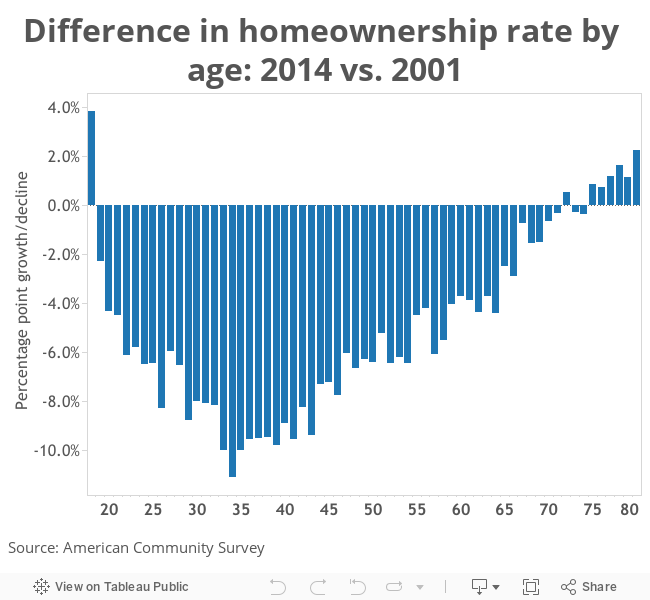

But it’s also clear that at every age below 60, homeownership rates are now significantly lower than they were in 2001. If we chart the difference itself, it looks like this:

For those aged 21 to 60, homeownership rates have fallen by six to 10 percentage points since 2001. The biggest declines have been for those in their thirties. (Note, too, that while some accounts make sharp distinctions between generations, this chart shows how continuous and consistent is the relationship between age and the decline in housing tenure, with the behavior of the oldest millennials flowing into that of the youngest gen-Xers.)

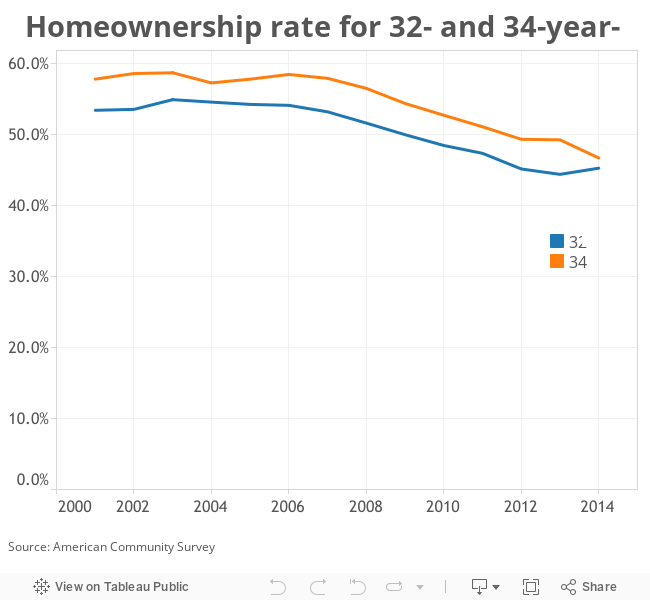

To distinguish between a lifecycle change and generational change, it can also be helpful to focus on a single age group over a long period of time. In the following chart, we look at the homeownership rates of 32-year-old and 34-year-old heads of household in each year from 2001 to 2014.

There are two obvious takeaways. First, 34-year-olds are more likely to be homeowners than 32-year-olds (the blue line is higher than the red line). Second, over time, the homeownership rate of both 34-year-olds and 32-year-olds has gone down (both lines slope down to the right). Again: This signals a generational change in home buying tendencies. Both 32- and 34-year-olds are less likely in 2014 (by a wide margin) to be homeowners than they were in 2001. And if there were evidence that in the last few years millennial home buying tendencies were reverting to those of previous generations, it would show up here, as a reversal or upswing in these lines. But they continue to slope down, indicating that homeownership, far from rebounding to historic patterns, is continuing to become less common among this generation than its predecessors.

We can use the change in age-specific home-ownership propensities to compute how many fewer millennials own homes today than would have been the case if they had behaved as previous generations did. To do this, we multiply the 2001 home-ownership rate for each age group by the number of household heads in 2014, and compare the the predicted number of homeowners in each age group with the actual number reported by the census. The calculation is shown in the following table. In all, we estimate that there are 1.7 million fewer millennial home-owning households today than would have been the case if homeownership were as prevalent today as it was in 2001.

“Just delaying” homeownership results in big change in real estate

Finally, there’s a statistical claim being made here that Millennials are just like other generations in their home buying habits and preferences, they’re just buying homes and moving to the suburbs later in life. There are two problems with this argument. First, a one- or two-year change in the average age of first home purchase significantly reduces the number of homeowners permanently. It automatically means that those who own homes will be homeowners for about 2.5 to 3 percent less of their lifetime—over the whole population, over several decades that translates into a permanent decline in the homeownership rate. Second, the implication is that somehow, though they wait longer to buy their first home, eventually, they’ll catch up to historic levels of homeownership . . . someday. But there’s no evidence for this “catch up” theory—in fact, homeownership levels are dropping for everyone up through about age 60. American’s are both delaying homeownership until they’re older, and buying fewer homes over their lifetimes—which together represent a huge change in how US housing markets work.

Far from debunking the story about Millennial home-buying habits being different, the latest data confirm that serious, long-term changes are afoot. We’re well past the dark days of the 2009 recession. The economy has been growing again for six years, and home buying rates at all ages remain depressed well below historic levels—no more so that for those Millennials in their mid-30’s who are fully ten-points less likely to be homeowners than the Gen-Xers of 2001 were in their mid 30s.

Data Notes:

These data are taken from the American Community Survey for the years indicated. There are many different definitions of what constitutes the “millennial” generation: for these tabulations we follow NARs definition of those born between 1980 and 2000.