What City Observatory Did This Week

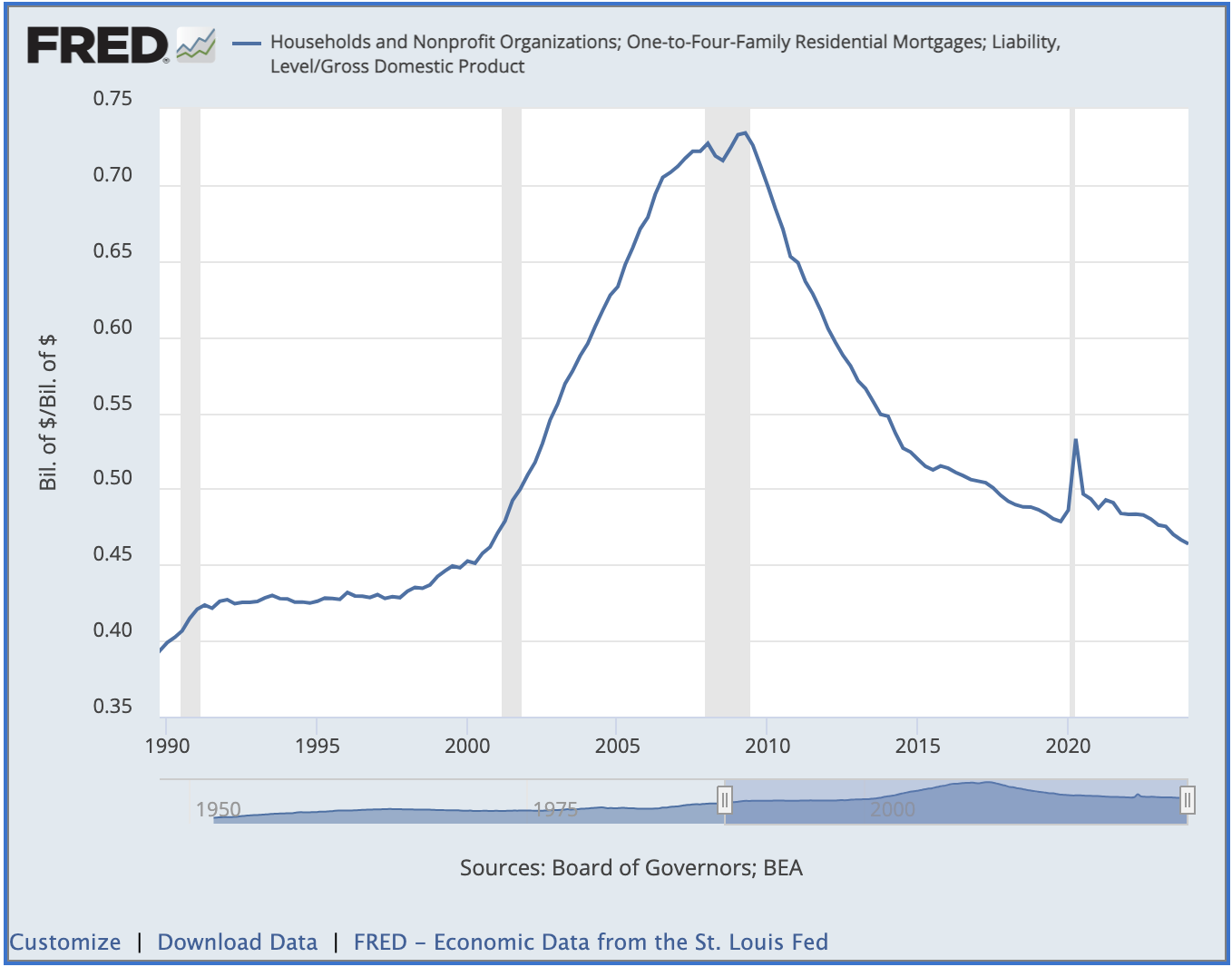

There’s no evidence of a housing bubble. Strong Towns Chuck Marohn has a recent blog post proclaiming that the US housing market is the midst of another bubble, similar to 2008. But a closer look at housing market fundamentals, especially mortgage debt, shows few parallels to that earlier debacle.

- Mortgage debt to GDP ratio is declining, unlike the surge seen before 2008.

- Lending standards are stricter now, with most mortgages going to households with good credit.

- The median FICO score for new mortgages is high (770), and few loans go to those with scores below 620.

- Most homeowners have significant equity and affordable fixed-rate mortgages.

- Adjustable-rate mortgages now require borrowers to qualify based on higher potential payments.

- Mortgage fraud, while still present, has declined significantly since the previous bubble.

To be sure, housing prices are high and affordability is an issue. However, the underlying problem is insufficient housing supply, particularly in high-demand urban areas, rather than a bubble caused by “financialization.” Labeling the current situation a “bubble” doesn’t accurately describe the problem or help in finding solutions. Instead, the focus should be on addressing supply constraints, especially in desirable locations.

Must Read

David Zipper: Moving past the proof of induced travel to change investment priorities. It’s well proven that wider highways simply induced more travel, meaning that the billions spent on wider roads don’t solve congestion and make pollution and climate problems worse. David Zipper has a comprehensive, long-form essay that strives to take us past the demonstrated science of induced travel to practical political advice on how to change spending priorities.

Zipper points to the 1980s era alliance between environmentalists and fiscal conservatives which resulted in slashing massive federal subsidies for dam-building. It’s a tempting analogy, because there’s clearly a need to break political stranglehold the highway-industrial complex has on “infrastructure funding.” In a way, though, there’s a more germane example from the freeway fights of the sixties and seventies. Federal legislation then allowed state and local governments to “withdraw” federal funding for proposed freeways, and apply it for other transportation priorities. A similar program today–with bonus funding for moving money away from highways, and towards transit, biking and walking–might encourage states to rethink their priorities. As it is, the federal government is now doing much the opposite, giving “bonus” funding for big highway projects, like Cincinnati’s Brent Spence Bridge and the I-5 Bridge Replacement in Portland. More flexibility, coupled with bonus funding for the kinds of “green” transportation projects that we want to see could also break the highway addiction.

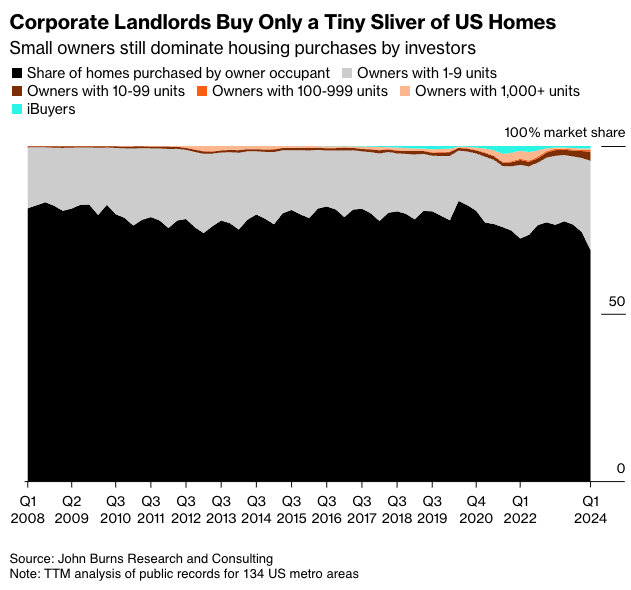

The myth of corporate landlords. One of the favorite boogeymen of the housing debate is the idea that rents are rising because Wall Street is buying up homes. But the truth is large scale investors account for a trivial fraction of home owners. Housing experts at the Urban Institute have labeled the idea baseless scapegoating. An article at Bloomberg Business Week casts serious statistical doubt on the idea that corporate investors play an important role in moving housing markets. The data show that most investors are “mom and pop” landlords who own fewer than 10 units.

Most of these investors are very small scale, not the hedge funds or Wall Street firms that are typically cast as villains:

“The opposition to investment in single-family homes is often misguided,” says Tawan Davis, CEO and founder of the Steinbridge Group, an employee-owned real estate investment firm. “Only 2 to 3% are owned by Wall Street; 95% are second homes, inherited homes, or small real estate owners.”

New Knowledge

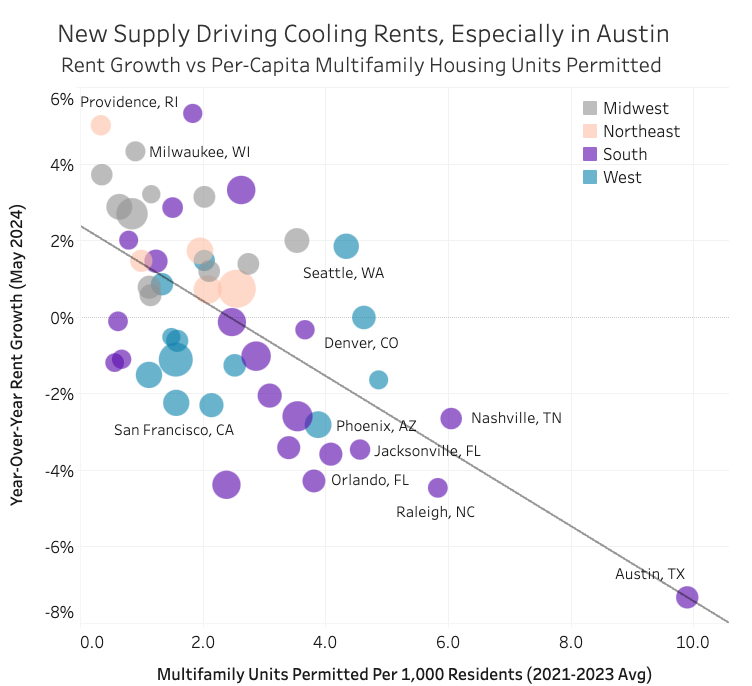

More apartments equal lower rent inflation. ApartmentList.com has its finger on the pulse of housing markets across the country, and their latest data shows that the markets that built the most apartments in the past year or so have had the lowest rates of rental inflation. Over the past year, rents actually declined in about half of all major metro markets; systematically, these were the markets that had the fastest growth in multi-family permitting over the previous two years. Simply, more supply helps hold down or drive down rents.

This is simple and important truth that is too often overlooked in housing debates. If we want to keep housing affordable, or make it more affordable, we need to build more of it.