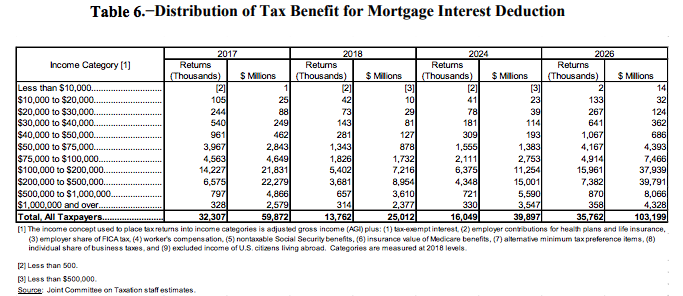

Tax changes cut the Mortgage Interest Deduction sharply–but not for the rich

The 1.2 percent of households with incomes over $500,000 get 20 times as much tax relief from the mortgage interest deduction as the half of all households with incomes under $50,000.

Every year, the federal government spends about $250 billion on subsidized housing–not for the poor, mind you, but in the form of tax breaks for homeownership.

While a lot of attention gets focused on the mortgage interest deduction (MID), it’s just one of four major provisions in the tax code that subsidize homeownership. The others include the state and local tax deduction, the favorable capital gains treatment of housing, and the exclusion from income of the imputed rent that owners reap from living in their homes.

The Tax Cuts and Jobs Act of 2017 pares back the scope and benefits of the mortgage interest deduction. By raising the standard deduction and capping the size of mortgages on which taxpayers can deduct interest payments, Congress greatly reduced the number of households that are likely to claim the deduction, and also reduce their tax savings. The Joint Committee on Taxation estimates that the number of households that will claim the MID in 2018 will be 13.8 million, less than half the number who are claiming it in 2017.

These changes will reduce the size and cost of the MID. Total taxpayer savings from the MID are expected to fall from $59.9 billion in 2017 to just $25.0 billion in 2018.

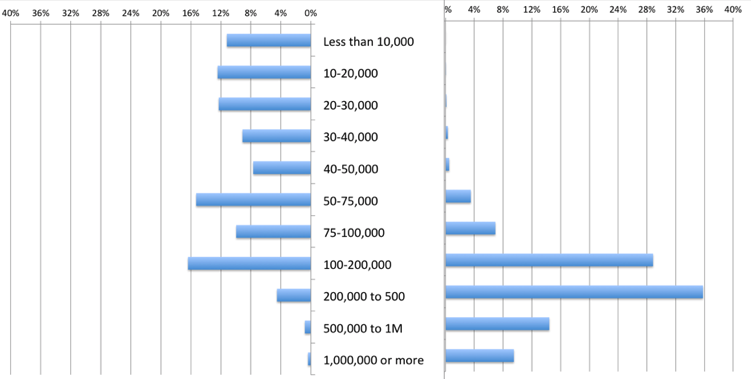

But while the total cost of MID goes down, the benefits of MID shift even more heavily to the highest income households. The tabular presentation of this data is a little opaque, so we’ve converted it into a graphic format. For comparative purposes, we’ve shown the share of households in each taxable income category (from 2017). The chart below shows the distribution of households by income level (on the left hand side of the chart) with the distribution of the value of the mortgage interest deduction by income level in 2018 (on the right hand side of the chart).

Households by Income Level Mortgage Interest Deduction Tax Savings

It’s apparent that the benefits of the MID are heavily skewed to high income households, and are essentially non-existent for low and middle income Americans. Half of all households had incomes of less than $50,000 per year; they get about one percent of the tax benefits from the mortgage interest deduction. At the other end of the spectrum, the top 1.2 percent of households by income get 25 percent of all of the tax benefits from the mortgage interest deduction. Thus, households with incomes of more than $500,000 per year get about 20 times more benefit from the mortgage interest deduction than the half of all households with incomes under $50,000.

The mortgage interest deduction has always been structured to benefit upper income Americans. Fundamentally, you had to be a homeowner to get any benefit, and as a group, the nation’s renters have lower incomes than homeowners, meaning they got nothing. Among those who could purchase a home, benefits were larger for the rich: The more money you borrowed and the higher your tax bracket, the bigger a tax benefit you got from MID. The changes to the tax law approved last year skew the distribution of gains even further in favor of the rich. While about 50 percent of the benefits of the MID went to households with incomes over $200,000 in 2017, roughly 60 percent of the benefits of MID go to such high income households in 2018.