Lingering racism holds down property values in majority black neighborhoods

For most American households, their home is their largest financial asset; how valuable that asset is, and whether it appreciates has a profound impact on a household’s financial well-being. Unsurprisingly, a big component of the racial wealth gap in the United States has to do with differences in rates of homeownership, and also in the value of homes owned by black and white households.

There’s a profound gap between the value of homes in majority black and predominantly white neighborhoods in the nation’s metropolitan areas, according to estimates from the Brookings Institution. Even after adjusting for home characteristics and neighborhood attributes, homes in majority black neighborhoods sell at a 20 percent or greater discount to otherwise similar homes in predominantly white neighborhoods.

The reasons for and implications of the value gap between white and black neighborhoods are complex. Lower value housing means incumbent homeowners have less wealth–but also implies that rents are lower and housing is more affordable in black neighborhoods than predominantly white ones. The devaluation of housing in black neighborhoods is primarily a result of the continued resistance many white homebuyers have to consider black neighborhoods, but also likely reflects the growing tendency of higher income black households to move to more suburban and integrated neighborhoods.

The Black/White Home Value Gap in Memphis

To get an idea of what this means in just one city, we look at the data for Memphis.

- Homes in majority black neighborhoods in Memphis are devalued by $2.3 billion compared to homes in predominantly white neighborhoods, according to estimates from the Brookings Institution.

- The typical home in a majority black neighborhood in Memphis sells for about $88,500, about $25,000 less than a similar house in a predominantly white neighborhood.

- Depressed values in black neighborhoods are correlated with lower wealth, but paradoxically may contribute to affordability.

These estimates come from a recent report from the Brookings Institution undertakes a detailed comparison of home prices in majority black neighborhoods compared to other neighborhoods in the United States. The report–The Devaluation of Assets in Black Neighborhoods— by Brookings scholars Andre Perry and David Harshbarger and Gallup’s Jonathan Rothwell uses home price data from 113 cities around the country and finds a consistent pattern of undervalued homes in majority black neighborhoods.

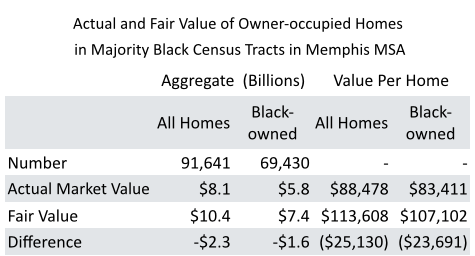

The Brookings Institution compared the sales value of owner-occupied homes in majority black neighborhoods with otherwise similar homes in exclusively white neighborhoods and found that the houses in black neighborhoods sold at a more than 20 percent discount to the homes in white neighborhoods. Here is a summary of the report’s findings for Memphis.

What this table means: This table shows that there are nearly 92,000 owner-occupied homes in majority black neighborhoods in the Memphis metropolitan area; of these, nearly 70,000 are owned by black homeowners. In the aggregate, these homes are worth about $8 billion, but would be worth more than $10 billion, if they were valued the same way as otherwise similar homes in similar, but predominantly white, neighborhoods. The typical home in a majority black neighborhood has a market value of about $88,000, which is about $25,000 less than a similar home in a majority white neighborhood.

The figures in this table reflect the difference in home values after controlling for house and neighborhood characteristics. The gross difference (without these controls) between home values in majority black neighborhoods and exclusively white neighborhoods is even larger. Majority black neighborhoods tend to be older, have smaller houses, and havefewer amenities and higher rates of poverty, compared to exclusively white neighborhoods. Perry and his colleagues used a regression analysis to statistically control for the effects of structural characteristics (home size, age, etc), and neighborhood characteristics (crime rates, schools, commuting distances). Even after adjusting for these effects–which explain some of the variation in home prices among neighborhoods–homes in majority black neighborhoods were still undervalued.

Economic Effects of Undervaluation

The data make a strong case that homes in majority black neighborhoods are systematically undervalued in comparison to otherwise similar homes in predominantly white neighborhoods. The magnitude of the disparity–the author’s estimate at $156 billion nationally–is also sizable.

The economic effects of this undervaluation are complicated and manifold. First, it is obvious that homeowners in these neighborhoods, most of whom are black, have less wealth than they otherwise would have if their homes commanded the same values as those in predominantly white neighborhoods. If it weren’t for this devaluation, homeowners in these majority black neighborhoods would have significantly greater home equity.

Beyond that, the picture is more complex, and the effects are mixed. For renters, lower home and property values probably mean they pay lower rents. And it could also be the case that these same homes have long been undervalued, meaning that while current owners have less equity than if they were fairly valued, they may also have paid a lower purchase price to acquire the property. The Brookings report is candid about these mixed effects:

. . . the devaluation of rental properties is advantageous to renters, in so far as it results in a lower rental payment for similar quality housing. The devaluation of owner-occupied housing makes it easier to acquire the home, but once purchased, it is unambiguously disadvantageous to the owner and occupier, who would otherwise benefit from being able to refinance, borrow, or sell at a higher valuation.

As we’ve often pointed out, there’s an inherent tension in US housing policy between affordability and wealth creation. Houses in majority black neighborhoods may be more affordable (i.e. sell at a discount to otherwise similar houses in predominantly white neighborhoods), but may therefore represent a loss of wealth for their owners.

What causes values to be depressed?

Why would otherwise similar houses in majority black neighborhoods sell for so much less than comparable houses in predominantly white neighborhoods? The first, and most obvious answer is the lingering effects of racism. Many white homebuyers may avoid searching in predominantly black neighborhoods, and the lower demand for housing in these areas causes prices to be lower. It is also likely that “steering” by real estate agents — directing white buyers primarily to white neighborhoods — also has this effect.

The decline in values is also likely compounded by the decisions of black homebuyers. Upper- and middle-income black households may rationally choose to buy homes in more integrated neighborhoods, not just for amenities like schools (which were arguably controlled for in the Brookings study), but also because they may believe that such neighborhoods will appreciate more. Over the past four decades, middle-income and higher-income black households have tended both to suburbanize and to integrate. According to Patrick Sharkey of New York University, a majority of black middle class households now live in the suburbs and almost as many lived in neighborhoods that are not majority black. In 1970, fewer than a third of middle- and upper-income African-American households lived in majority non-black neighborhoods; today it is more than half. In 1970, only about 20 percent of middle-and upper-income households lived in suburbs; today it is nearly half.

The exit of upwardly mobile black households from majority black neighborhoods has increased economic polarization according to David Rusk of the D.C. Policy Center. Similarly, the relatively low prices of homes in majority black neighborhoods may mean that these are the only locations that black households with more modest incomes can afford. The net result may be that lower-income homeowners become more concentrated in majority black neighborhoods. The movement of many black households out of majority black neighborhoods–particularly those households with means–coupled with the continued tendency of white households not to purchase in such areas likely both contribute to the housing price disparities observed in the Brookings report. Finally, as the report points out, the low value of homes in majority black neighborhoods means that homeowners there have less equity in their homes and therefore may find it difficult or impossible to sell and move to a different neighborhood.

Housing prices, like those of other investments, reflect not just the current utility or value of assets, but also the expected return. Buyers will pay more for housing in areas they expect will appreciate. Robert Shiller has shown that variations in buyer expectations of future home price appreciation play a key role in the formation of housing bubbles. The same tendency is likely to play out across neighborhoods in metropolitan areas: Neighborhoods that are perceived as up and coming are likely to have a different price trajectory than neighborhoods that are seen as stagnant or declining.

One finding that these data suggest is that whites are paying a premium to live in all-white neighborhoods. One implication of the substantial (20 percent plus) differential in home values between comparable houses in majority black and nearly all white neighborhoods is that white households are foregoing the opportunity to get a much less expensive home by buying in a black neighborhood. Because some white households may be much less averse to having black neighbors, some of what we see as gentrification may be propelled by the substantially lower cost of housing in majority black neighborhoods.

Tomorrow, in part 2 of this series, we’ll take a further look at this issue of wealth disparities, and focus on how housing values in black and white neighborhoods have changed over time, and what challenges that closing this gap poses for policymakers.