The greater San Francisco Bay area has been a hotbed of economic activity and technological change for decades, bringing us ground-breaking tech companies from Hewlett-Packard and Intel, to Apple and Google, to AirBNB and Uber. Its a great place to spot trends that are likely to spread elsewhere. One such trend is the growing tendency of new technology startups to locate in cities. Today we explore some new data on venture capital investment that are indicative of this trend.

As we noted in July, there’s always been a dynamic tension between the older, established city of San Francisco in the north, and the new, upstart, tech-driven city of San Jose in the south. From the 1950s onward, San Jose and the suburban cities of Santa Clara county grew rapidly as the tech industry expanded. Eventually the area was re-christened Silicon Valley.

One of the hallmarks of the Valley’s growth was the invention and explosion of the venture capital industry: Technology savvy, high risk investors, who would make big bets on nascent technology companies with the hopes of growing them into large and profitable enterprises. Sand Hill Road in Palo Alto became synonymous with the cluster of venture capital that financed hundreds of tech firms.

Silicon Valley’s dominance of the technology startup world was clearly illustrated each year with the publication of the dollar value of venture capital investments by the National Venture Capital Association and PriceWaterhouseCoopers MoneyTree. Silicon Valley startups would frequently account for a third or more of all the venture capital investment in the United States. But since the Great Recession that pattern has changed dramatically.

By 2010, according to data gathered by the NVCA, the San Francisco metro area had pulled ahead of Silicon Valley in venture capital investment. In the past two years (2014 and 2015) venture capital investment in San Francisco has dwarfed VC investment in Silicon Valley. In 2015, San Francisco firms received about $21 billion in venture capital investment compared to about $7 billion in Silicon Valley.

VC investment is important both in its own right–because we are talking about billions of dollars, which gets spent on rent, salaries and other purchases, initially at least in these local economies–but perhaps more importantly because venture capital investment is a leading indicator of future economic activity. While individual firms may fail, the flow of venture capital investment is indicative of the most productive locations for new technology driven businesses.

What these data signal is that it is an urban location–San Francisco–that is now pulling well ahead of Silicon Valley, which is still mostly characterized by a suburban office park model of development. Some of this may have to do with the kind of firms that are drawing investment. Much of the current round of VC investment is going to software and web-related firms, not the kinds of semiconductor-driven hardware firms that have been Silicon Valley’s superstars in the past. But unlike the 1970s and 1980s, when technology was a decidedly suburban activity, focused primarily in low density “nerdistans,” today its the case that new technology enterprises are disproportionately found in cities. And today, companies are increasingly choosing to locate their operations in more urban neighborhoods and more walkable suburbs.

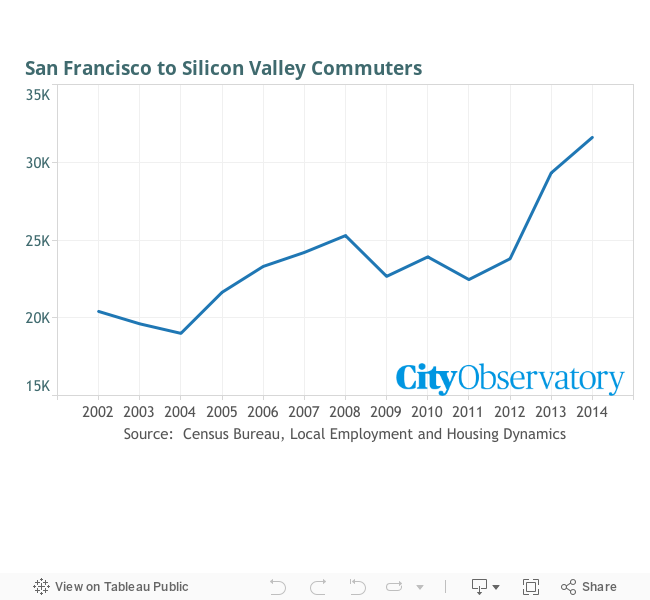

What’s driving firms to cities is the fact that the workers they want to hire–well educated young adults in their twenties and thirties–increasingly want to live in dense, walkable urban environments like San Francisco, and not the sprawling suburbs of Silicon Valley. Further evidence of this trend is, of course, the famous “Google buses” that pick up workers in high-demand neighborhoods in San Francisco and ferry them, in air-conditioned, wifi-enabled comfort, to prosaic suburban office campuses 30 or 40 miles south.

The movement of workers, investment, and new startup firms to San Francisco is another indicator of the growing strength of cities in shaping economic growth. And has been the case over the past half-century or more, trends that start in the Bay Area tend to ripple through the rest of the country. What we see here is a shift in economic polarity, from the suburban-led growth of the past, to more city-led growth. That’s one of the reasons we think the reversal of the long process of job decentralization has just begun.

Finally, some background about geography. The Bay Area has several major cities, including San Francisco, Oakland and San Jose. To the Office of Management and Budget, which draws the boundaries of the nation’s metropolitan areas after each decennial census, the three cities were all part of a single metropolitan area up through the classification created following Census 2000. In 2010, with new data, and slightly different rules for delineating metro areas, San Jose was split off into its own separate metropolitan area, consisting of Santa Clara and San Benito counties at the south end of San Francisco Bay. (If it hadn’t been hived off into its own metro area, the name of the larger metropolis would have been the “San Jose-San Francisco-Oakland” metropolitan area, inasmuch as the city of San Jose’s population had passed that of San Francisco.