Over the past year, rent inflation has declined in 48 of the top 50 markets

For the past several years, rising rents have been at the center of the nation’s housing affordability debate. A combination of former homeowners dispossessed by the collapse of the housing bubble, weak incomes and job prospects for younger workers and a growing demand for urban living have increased the demand for rental housing in the face of a relatively slowly changing supply of apartments and rental houses. Particularly in hot coastal markets, like San Francisco, Seattle, New York and Washington, rents have been rising much faster than inflation.

Spiking rents have produced a predictable demand for policy solutions, ranging from inclusionary housing mandates to rent control. Economists–ourselves included–have long counseled that the most important ingredient to achieving a reduction in rental inflation was an increase in housing supply. A critical challenge is the temporal mismatch between supply and demand. The demand for housing can change relatively rapidly, with changes in employment, migration and tastes. Building new housing takes time: prospective developers have to recognize a need, arrange financing, secure planning permission, and then actually construct new units. Its common for demand to outstrip supply in the short term.

Not surprisingly, those confronted with the burden of paying ever higher rents have little comforted by economists lecturing them about the long run benefits of increased supply. And some have even counseled economists to keep their mouth’s shut and not talk about housing markets in terms of supply and demand. At City Observatory, we’ve been looking for teachable moments to make the case for basic economic principles. In the past few months, we’ve pointed out some examples of markets where rental rates have been moderating. But its worth taking a look across the nation to judge the trends.

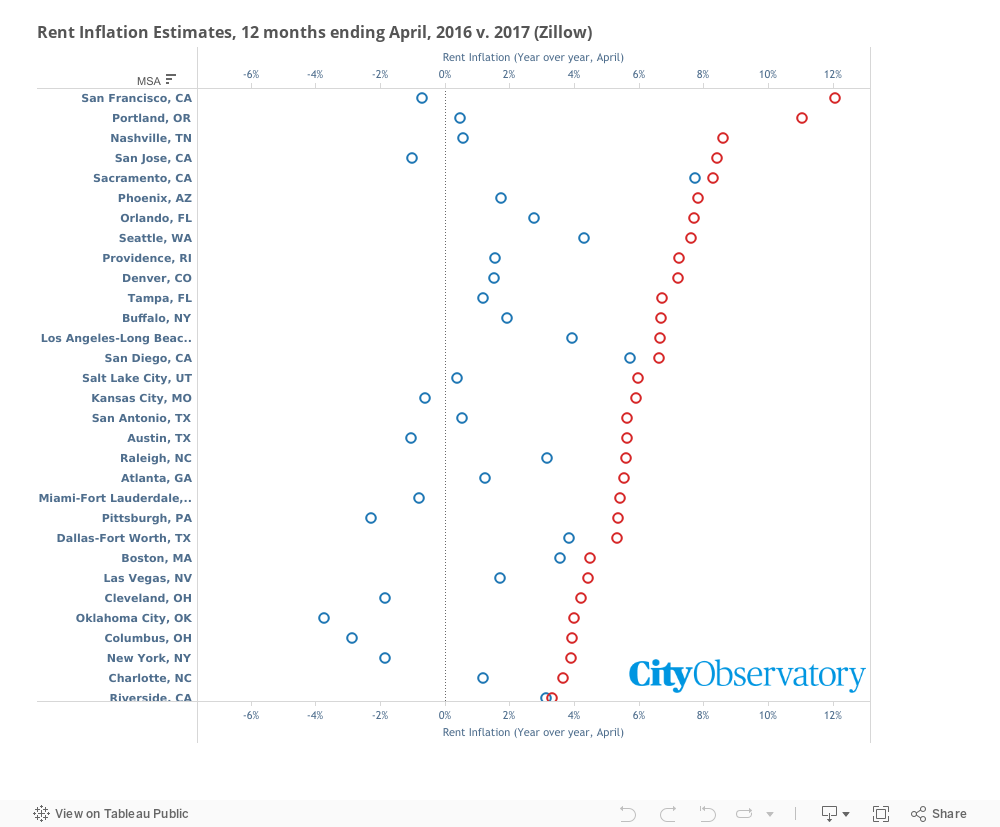

Today there’s growing evidence that in rental markets across the nation that supply is catching up with demand, and that rent hikes are moderating everywhere. Rents are actually falling in some cities. The latest data from Zillow tracks changes an multifamily rents on a monthly basis for the nation’s metropolitan areas. We look at the 12 month change in prices between April 2016 and April 2017 (the last twelve-0month period for which data are available) and compare it to the change in rents in the preceding 12 months (April 2015 to April 2016). In the following chart, blue dots indicate the rate of rental inflation in the past 12 months (April 2016- April 2017), and red dots indicate the rental inflation in the preceding 12 months (April 2015-April 2016). Metro areas are ranked in order of their rate of rental inflation in the earlier time period.

First, the most striking finding: Rental inflation was lower in the past 12 months in 48 of the 50 largest metro markets. Only in Hartford and Cincinnati did rents increase more in the past 12 months than in the period between April 2015 and April 2016. The deceleration was particularly sharp in most of the markets with the highest rates of rental inflation in 2015. San Francisco’s rent inflation dropped from 12 percent to -0.7 percent. Portland’s dropped from 11 percent to 0.5 percent.

Second, in 20 of the top 50 markets, rents actually declined in the past 12 months. Year-over-year, rents dropped in San Francisco, New York, Austin and Miami. There’s a certain asymmetry to reporting on rent data: Rent increases merit headlines; rent decreases generally don’t.

Third, looking forward, its possible, if not actually likely that rental inflation could soften further. Even more housing units are coming on line in the next year or two.

The combination of more supply and continuing (if slow) improvements in income are likely to lessen the nation’s housing affordability problems. Already, according to the Joint Center for Housing Studies, the share of rental households who were cost-burdened (i.e. spent more than 30 percent of their income on housing) declined from 49 percent in 2014 to 48 percent in 2015.

We’ll keep following the data on rental price trends in the months ahead. The good news for the moment is that the economist’s prediction appears to be right: As more supply comes on the market, we should expect rental inflation to subside. Stay tuned.

This post has been revised to correct an earlier mistaken reference to the colors of the dots identifying the two time periods. Thanks to our sharp-eyed readers for pointing out the error.