The wealth of black families lags far behind whites, and housing markets play a key role

There’s a great article from The New York Times’ Emily Badger about a new study that shows just how much Americans (especially white Americans) underestimate the gap in the economic circumstances between black and white families. The study also makes the point that we tend to greatly overestimate the amount of progress that’s been made in closing that gap.

The Times’s story is based on research by Yale’s Michael Kraus, Julian Rucker and Jennifer Richeson, entitled “Americans misperceive racial economic equality.” Their paper that compares a series of surveys about perceptions of earnings, income and wealth gaps between blacks and whites with data gathered by the Census Bureau. The headline finding is that the average respondent thinks that black wealth is about 80 percent that of whites; whereas Census data suggest that black wealth is about 5 percent that of whites.

Let’s zero in for a moment on the question of the wealth disparity. While we have multiple measures of income, we have actually relatively few measures of the wealth of American households. One survey conducted by the Census Bureau (the Survey of Income and Program Participation, SIPP) asks questions about financial holdings and debts. The other survey is undertaken on a triennial basis by the Federal Reserve Board (the Survey of Consumer Finance, SCF). The SCF asks more detailed questions about investments, banking, credit, automobile and home ownership and related issues. There’s actually a terrific analysis by the Federal Reserve’s Jeffrey Thompson and Gustavo Suarez, entitled “Exploring the Racial Wealth Gap Using the Survey of Consumer Finances,”

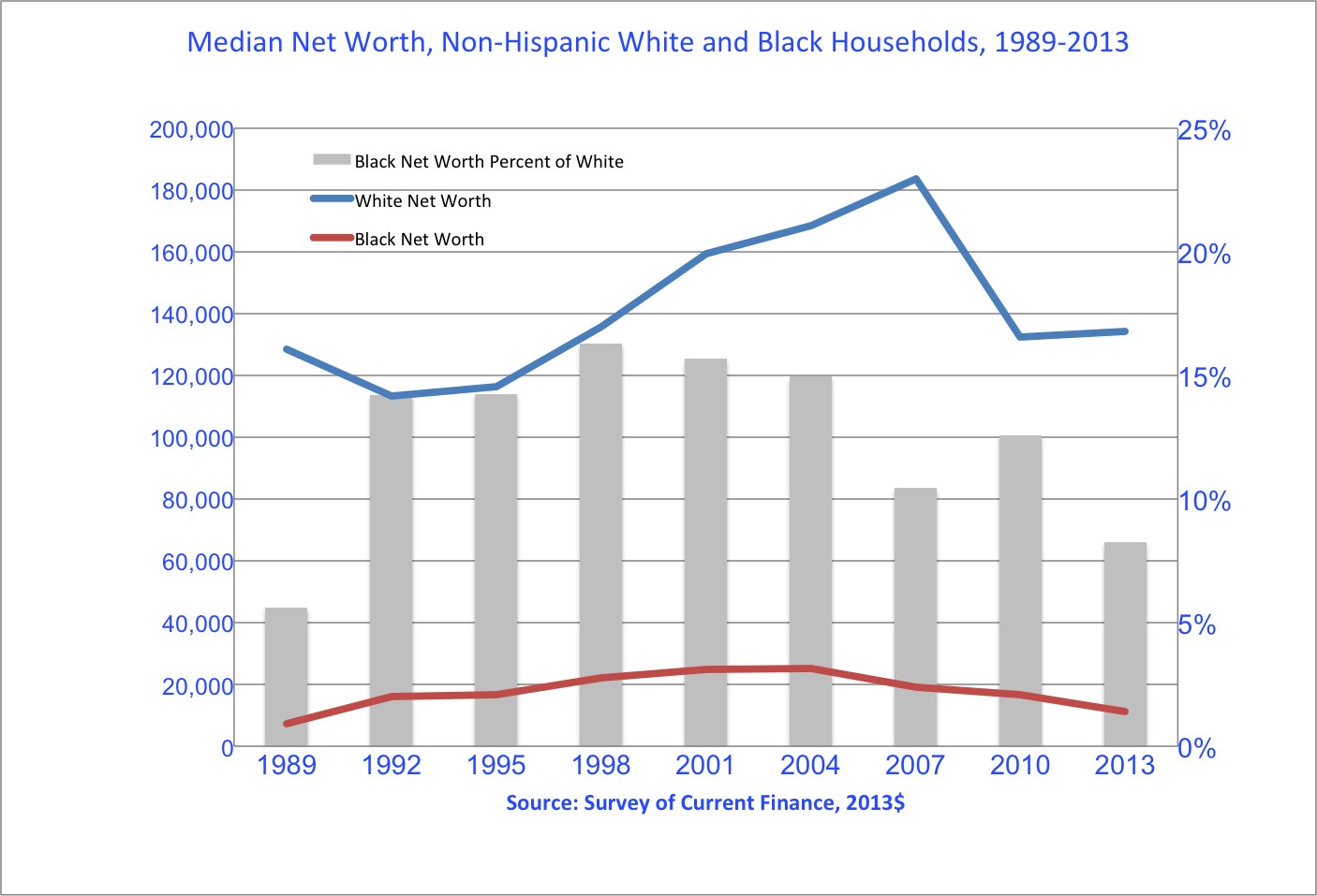

We’ve plotted data from the Thompson & Suarez report for the period 1989 through 2013 to chart the median net worth of black and non-Hispanic white households. The data are shown in 2013 dollars. The red line corresponds to the net worth of black households; the blue line non-Hispanic white households (values on the left axis) and the gray bars show median net worth of black households as a percentage of the median net worth of non-Hispanic white households (measured on the right axis).

A couple of observations: First: as of 2013, the net worth of the typical household hadn’t rebounded to pre-recession levels. This was true for white and black households alike. But the decline for black households was proportionately greater than for whites. The median net worth of black families fell 42 percent, from $19,200 in 2007 (on the eve of the Great Recession) to $11,100 in 2013. The median net worth of white families decline as well, but by only 27 percent, from $183,500 in 2007 to $134,100 in 2013.

Second, as we look back at the longer historical record it was quite clear that during the 1990s in particular, black households were actually closing the wealth gap with their white counterparts. In 1989, the typical black household had a net worth than was only 5.6 percent of the typical white household. By 1998, black households net worth was 16.3 percent of that of whites. Black households treaded water during the early years of after 2000, and have clearly lost ground relative to whites in the wake of the Great Recession. Today average black wealth stands at just 8.3 percent that of whites. (This figure is slightly higher than the 5 percent reported in The New York Times story; excluding the value of owner-occupied homes, the SIPP reports that black wealth is about 5.3 percent that of white households in 2013.)

So what’s the explanation?

A lot of this has to do with housing markets, housing policy and the housing cycle. Households with good access to credit prior to the housing bubble were in the best position to profit from the run up in house prices (and note that white net worth outpaced black from 2001 onward). As we’ve explained at City Observatory, low income households generally, and households of color in particular tend to suffer from bad market timing: buying a home later in the housing cycle (when prices were higher) exposed them to more risk when housing markets collapsed. Moreover, housing is a larger fraction of the net worth of low income households and households of color, so when housing prices went down, they were harder hit that the typical white household (which had a much more diversified wealth portfolio).

There’s also an important spatial bias in black household homeownership. Black households tend to buy and own homes in neighborhoods with greater price volatility, especially on the downside. As Zillow demonstrated, the housing bust produced sharper and more sustained declines in home prices for households of color than for whites.

The takeaway–while it’s certainly true that white households have a huge (and widely under-estimated) edge in wealth, it’s not the case that we have not made progress. The decade of the 1990s stands out as a period in which the wealth of black households increased significantly relative to their white counterparts. What’s remarkable is that the housing bubble and the Great Recession essentially erased all of the relative gains in black household wealth from the 1990s. The lesson of the last twenty years seems to be that encouraging greater homeownership is not just ineffective in reducing the racial wealth gap, but is actually counterproductive.

And there’s a post-script here: As startling as the wealth gap is between blacks and whites, its even sharper between owners and renters. According to the Census Bureau, the median net worth of a homeowner in the United States was $199,600. The median net worth of renters is $2,200, barely one percent of that amount. This disparity speaks strongly to the subsidies and tax preferences for housing as an investment. But it also shows that we have little if anything to offer in the way of a wealth-building strategy to the third to forty percent of the nation’s households who rent their homes. Given the financial perils of encouraging homeownership for those with modest incomes, we ought to be devoting more attention to mechanisms to help families build wealth without having to go long in the real estate market.