If you believe the soothsayers–including the CEO of Lyft–our cities will soon be home to swarms of autonomous vehicles that ferry us quietly, cleanly and safely to all of our urban destinations. The technology is developing–and rolling out–at a breakneck pace. Imagine some combination of Uber, electrically powered cars, and robotic control. You’ll use your handheld device to summon a robotic vehicle to pick you up, then drop you off at your destination. Vast fleets of these vehicles will flow through city streets, meeting much of our transportation demand and reducing the ownership of private cars. Big players in the automobile and technology industries are making aggressive bets that this will happen. But, the big question behind this, as we asked in part one of this series yesterday, is “how much will it cost?”

While the news that Uber is now street-testing self-driving cars in Pittsburgh–albeit with full time human supervisors–has heightened expectations that a massive deployment is just around the corner, some are still expressing doubts. The Wall Street Journal points out that the initial deployment of autonomous vehicles may be restricted to well-mapped urban areas, slow speeds (under 25 miles per hour) and good weather conditions. It could be twenty years before we have “go anywhere” autonomous vehicles.

And those looking forward and contemplating the widespread availability of self-driving cars are predicting everything from a new urban nirvana to a hellish exurban dystopia. The optimists see a world where parking spaces are beaten into plowshares, the carnage from car crashes is eliminated, where greenhouse gas emissions fall sharply and where the young, the old and the infirm, those who can’t drive have easy access to door-to-door transit. The pessimists visualize a kind of exurban dystopia with mass unemployment for those who now make their living driving vehicles, and where cheap and comfortable autonomous vehicles facilitate a new wave of population decentralization and sprawl.

To an economist, all of these projections hinge on a single fact about autonomous vehicles that we don’t yet know: how much they will cost to operate. If they’re cheap, they’ll be adopted more quickly and widely and have a much more disruptive effect. If they’re more expensive than private cars or transit or biking or walking, they’ll be adopted more slowly, and probably have less impact on the transport system. (It’s worth noting that despite their notoriety, today’s Uber and Lyft ridesharing services have been used by less than 15 percent of the population). Whether autonomous vehicles become commonplace–or dominant–or whether they remain a niche product, for a select segment of the population or some restricted geography, will depend on how much they cost.

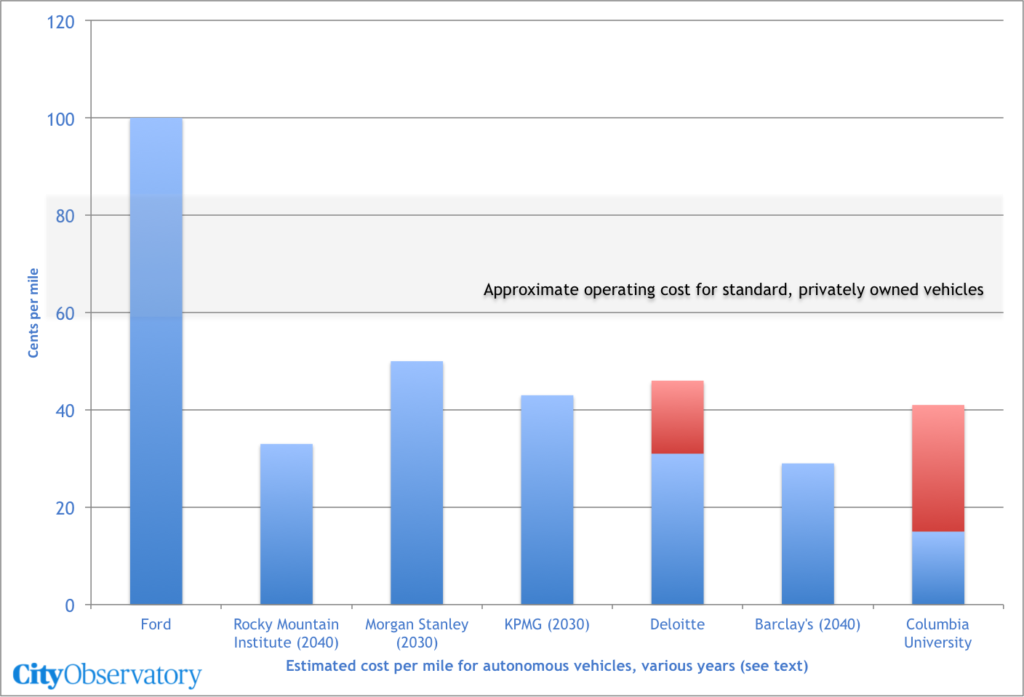

As we reported yesterday, the consensus of estimates is that fleets of autonomous vehicles would likely cost between about 30 and 50 cents per mile to operate sometime in the next one to two decades. That’s potentially a good deal cheaper than the 50 to 85 cents average operating cost for a conventional privately owned vehicle. All of these estimates assume that the hardware and software for navigation and vehicle control, including computers, sensors and communications, though expensive today, will decline in cost as the technology quickly matures. Some of those savings come from a combination of electric propulsion, and perhaps smaller, purpose built “pod” vehicles. But most of the savings comes from greater utilization. Privately owned cars, it is frequently noted generally sit idle 90 percent of the time. In theory, at least, fleets of autonomous vehicles would be more nearly in constant motion, taking up less space for storage, and doing more work.

Peak demand and surge pricing

A couple of things to keep in mind as we ponder the meaning of these estimates: First, cost is not the same as price. While these figures represent what it might cost fleet owners to operate such vehicles, the prices they charge customers will likely be higher, both because they’ll want a profit, and because travel demand at some peak times (and locations) will exceed capacity.

And that’s the big obstacle to realizing the theoretical higher utilization of autonomous vehicles. Demand for travel isn’t spread evenly throughout the day. Many more of us want to travel as certain times (especially early in the morning and late in the afternoon) and the presence of these peaks, as we all know, is the defining feature of our urban transportation problem. Whiz-bang technology or not, there simply won’t be enough autonomous vehicles to handle the demand at the peak hour, for two reasons: first, fleet operators won’t want to own enough vehicles to meet the peak, as those vehicles would be idle all the rest of the time. The second issue is what Jarrett Walker has called the “geometry” problem: there simply isn’t enough room on city streets and highways to accommodate all the potential peak travelers if they are each in a personal vehicle.

Consider a practical example. One prominent study, by Columbia University’s Earth Institute, predicts that it would be possible to run autonomous vehicles in Manhattan for 40 cents per mile. That’s far cheaper than current modes of travel–including taxi, ridesharing, private cars and even the subway or bus for trips of less than five miles–so it’s likely that many more people will want to take advantage of autonomous vehicles than there will be vehicles to accommodate them. So, at the peak, autonomous vehicles will undoubtedly charge a surge fare, just Uber and Lyft do now.

The competitive challenge to transit, especially off-peak

Most of the estimates presented here suggest fully autonomous vehicles will be cheaper than privately owned conventional vehicles. It’s also likely that they may be less expensive than transit for many trips. In many cities the typical bus trip is only 2 or 3 miles in length; if the price of an autonomous vehicle is less than 50 cents per mile, the cost of such a trip (door-to-door, in an non-shared vehicle) will be less than the transit fare. Autonomous vehicles could easily cannibalize much of the transit market, especially in off-peak hours.

And because they can charge fares much higher than costs at the peak, operators will likely discount off-peak fares to below cost. That may mean at non-peak times, autonomous vehicles may be available to travelers at prices lower than the estimates shown here. Simply put, as long as operators cover their variable costs–which are likely to be electricity and tires–they needn’t worry about covering their fixed costs (which can be paid for from peak period profits).

Behavioral effects of per-mile pricing

The silver lining here–if there is one–is that the kind of per mile pricing that fleet vendors are likely to employ for autonomous vehicle fleets will send much stronger signals to consumers about the effects of their travel decisions than our current mostly flat-rate travel pricing. Today, most households own automobiles, and have pay the same level of fixed costs (car payments, insurance) whether they use their vehicle or not for an additional trip. Because the marginal cost of a trip is often perceived to be just the cost of fuel (perhaps 15-20 cents per mile), households use cars for trips that could easily be taken by other modes. That calculus changes if each trip has a separate additional cost–and consumers are likely to alter their behavior accordingly. Per mile pricing will make travelers more aware–and likely more sensitive to–the tradeoffs of different modes and locations. The evidence from evaluations of car-sharing programs, like Zip-car, show that per mile pricing tends to lead many households to reduce the number of cars they own–or give up car ownership altogether.

The price of disruption

If these cost estimates are correction, and if autonomous cars are actually feasible any time soon, the lower cost of single occupancy vehicle travel and a different pricing scheme will likely trigger greater changes in travel behavior. At the same time, other institutions, like road-building agencies and transit providers may see a major disruption of their business models. A move to electric cars threatens the principal revenue source of road-building agencies, the gas tax. And an overall decline in vehicle ownership coupled with more intense peak demand could be a state or city transportation department’s fiscal nightmare. Whether that happens depends a lot on whether these forecasts of relatively inexpensive autonomous vehicles pan out.