Yesterday, we explored the differences in car insurance premiums in the nation’s largest metropolitan areas. Today, we will take a look at homeowners insurance rates. Unlike car insurance, homeowners insurance is not required in states. Still, this insurance can be required by a mortgage lender, and it is an important action to protect one’s home. Premiums vary across the US, with location being one of the strongest determinants of price. Differences in weather, proximity to disaster-prone areas, crime rates, and density can vary home insurance rates across different metropolitan areas. We will explore these variations in insurance premiums and consider how it might affect the overall cost of living.

Home insurance rates are important to examine right now because of the growing impact of climate change on our built environments. Differences in insurance costs among cities may become even larger in the years ahead. The growth in wildfires and extreme weather events associated with climate change has already produced record insurance payouts. Insurance models are generally based upon historical data. They calculate the expected payout and create prices accordingly. What happens when climate change shifts trends in unpredictable ways? Just last year, disaster payouts from reinsurers, the firms that insure the insurance companies, were the fifth highest in history. Climate change prompts insurance companies, and the “re-insurers” who share these risks to reevaluate their rate-setting models. When the risk for payout increases, so does the cost of insurance. Mother Nature plays a crucial role when considering insurance rates. Nature’s volatility can significantly heighten your premiums.

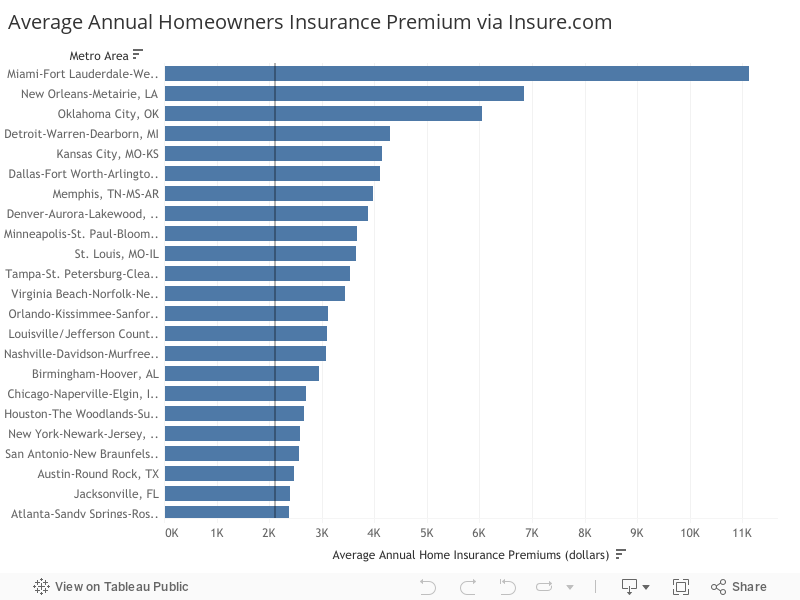

Which cities have the least (and most) expensive home insurance rates?

Home insurance rates have similar variables that impact the rates across the country. The greater the likelihood for damage to the home, the more expensive the rate will be. We used Insure.com data to compile the average annual home insurance rates across 52 of the largest metropolitan areas in the country. Unfortunately, Insure.com did not have any estimates for Riverside-San Bernardino-Ontario, CA. The site did not have clear methodologies on the rate, however, it was uniform throughout so we can examine the relative differences across these metro areas. Among the large metro areas, the median rate was $2118. (Cities have somewhat higher rates than rural areas, which is why the large city median is north of the national average of $1631).

The cities with the highest home insurance rates were Miami, New Orleans, Oklahoma City, and Detroit. The lowest home insurance rates were found in San Jose, San Diego, San Francisco, Sacramento, and Los Angeles. Among large metro areas, California appears to be the cheapest state to insure your home. In fact, with Seattle, Portland, and Las Vegas all below the 25th percentile as well, the West Coast proves to be a relatively inexpensive place to insure your home. The South? Not so much. Eight Southern cities are above the 75th percentile.

The risk of extreme weather in these regions appears to be a significant factor for these differences. Miami and New Orleans have hurricane seasons every year. In 2020, there were a record breaking 30 named hurricanes during the Atlantic hurricane season, with 11 landfalling in the United States. The risk for home damage due to the prevalence of events like this increases insurance rates. As climate change continues to disrupt the trends of the weather, we can expect home insurance rates to rise. Other regions also face their own unique risks: Oklahoma City is in a high risk zone for tornados, fires, and earthquakes. These natural disaster risks push up premiums. While there are wildfire and earthquake risks in the West, they haven’t produced dramatically higher insurance rates—yet. We will likely see changes in this over time as we continue to feel increasing impacts of climate change though.

Insurance and the Cost of Living

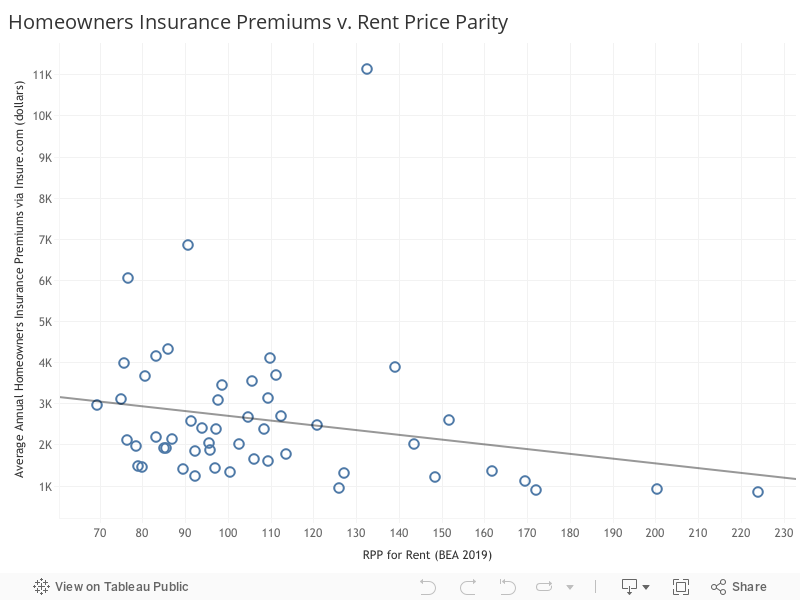

Just like we did yesterday for auto insurance, we compared the BEA’s RPP for Rent with the insurance data below. What we found: a slight negative correlation for homeowners insurance. However, when looking at the graph, you can see California standing out as an outlier, bringing down the correlation. When the RPP for Rent ranges from 80 to 150, there is a clear positive association between the insurance premiums and the price parity. This trend points us to consider that there might be an increasing effect for insurance rates and housing costs.

Let’s consider two cities: Oklahoma City and Seattle. According to Insure.com, the average annual homeowners insurance rate in Oklahoma City is $6045, while Seattle’s average rate is $1214. Clearly, there is a notable difference between these two premiums. When we compared the sprawl tax to cost of living, we used estimates of rent differential as a benchmark for cost of living. The cost of housing varies the most across metropolitan areas, so this was an effective measure for comparison. The typical resident in Oklahoma City paid roughly $2,525 less in annual rent/housing costs compared to the typical large metropolitan area. In Seattle, the typical resident paid approximately $2,055 more. From our Insure.com data, the annual housing insurance premium in Oklahoma City is $3,927 above the median premium across large metro areas. Seattle, on the other hand, has an annual premium that is $904 less than the median rate. These data suggest Oklahoma City’s high homeowner’s insurance rates effectively cancel out the lower rents in the metro area. The cost of housing is heightened significantly by homeowners insurance, placing Seattle and Oklahoma City on roughly the same pedestal. Seattle’s lower cost of insurance made up for the high rents. A cost of living comparison that omits these significant variations in insurance costs probably isn’t reliable.

What’s the relationship between home values and insurance rates? In general, we would expect that insurance premiums would be higher in cities with expensive housing, as it would be more expensive to repair or replace a home in an expensive metro than a lower priced one. Overall, there is a positive but modest relationship between home prices and insurance rates. Generally, the more valuable a home is, the more expensive it will be to insure it.

High homeowners premiums are likely to hike up the cost of living. However, low homeowners premiums in Western metro areas like Seattle, San Jose, and Sacramento at least partially offset higher annual housing costs. In contrast, some seemingly affordable Southern metro areas like New Orleans, Oklahoma City, and Memphis could have some or all of their affordability advantage eroded by notably high insurance premiums. These areas are where insurance makes its biggest impact in the overall cost of living.

Although homeowners insurance isn’t mandated by law like auto insurance, it is widespread and many homeowners regard it as essential, making it an important element to include in cost-of-living comparisons. Auto insurance likely plays a smaller role in the overall cost of living. Owning and insuring a car is not a requirement in all places, so the lack of need for auto insurance (and other car maintenance) could help lower the cost of living. It is difficult to fully quantify the cost of living across different areas because there is value in the external benefits of different cities. These cost of living comparisons struggle to encapture the amenities which cities can provide for their constituents. Still, insurance has the potential to play a mighty role in the cost of living. Auto and home insurance can require thousands of dollars out of consumers’ pockets each year. The impacts of climate change on our world will increase those premiums. Climate change is making a more volatile and uncertain world. As extreme weather risks intensify, the demand for insurance will as well. The role of insurance will heighten as we move into the future and it will be important to keep in mind how hefty the price tag is across the nation. The role in cost of living may not be entirely significant now, but as the world becomes more unpredictable, we could see the price to protect your belongings rise to new heights.

Note: This post has been updated to provide a link to insure.com‘s website.