The Oregon Department of Transportation is launching a series of boondoggle freeways, with no idea of their ultimate cost, and issuing bonds that will obligate the public to pay for expensive and un-needed highways.

Future generations will have to pay off the bonds AND suffer the climate consequences

The classic Robert Moses scam: Drive stakes, sell bonds

Debt is a powerful drug. Issuing bonds to pay for roads passes on to future generations the cost of the choices we make today. Once issued, repaying bonds takes precedence over any other use of state and federal highway funds. Launching a multi-billion dollar highway expansion plan in the Portland metro area jeopardizes the state’s ability to fund every other transportation priority, statewide, for the next two decades.

The Oregon Department of Transportation has embarked an unprecedented, multi-billion dollar highway expansion spree in Oregon. And they’re doing it without financing in hand, and instead are planning to issue bonds that will irrevocably commit the state to these projects, no matter how expensive or un-needed they may be.

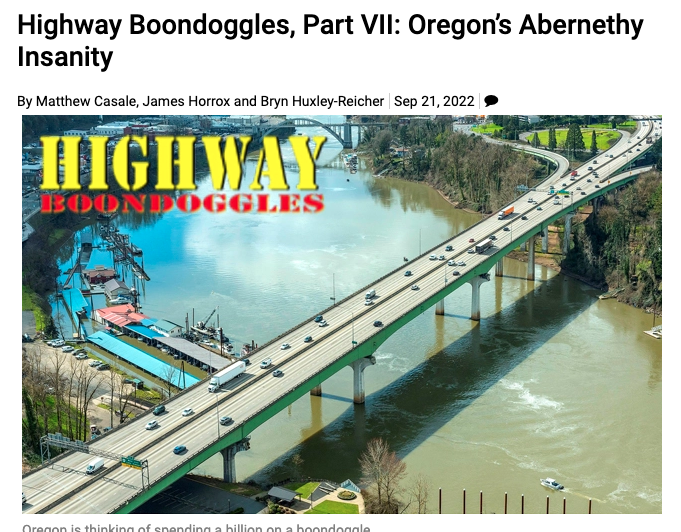

It has already started one project, the half billion dollar I-205 Abernethy Bridge, without permanent funding in place. The I-205’s bloated cost and minimal benefits have recently earned it national honors as a highway boondoggle:

And this is just one of several billion dollar plus projects for which ODOT is pursuing a build now, pay later approach. ODOT is moving forward with plans for the Interstate Bridge project, which it now admits could cost as much as $7.5 billion. It’s also trying to launch the $1.45 billion I-5 Rose Quarter project with only a tiny fraction of the needed funding. That’s nearly $10 billion in road construction. Significantly, the cost of every one of these projects has increased sharply in the past couple of years.

How can it do that?

First, ODOTit has figured that it once it starts these projects, no one will stop them. And it’s financing these projects by issuing debt. Its first step will be issuing up to $600 million in short-term bonds, secured by future state highway fund revenues. This short term borrowing is the government equivalent of a payday loan. They’re promising bond buyers first call on moneys in the state highway fund, hoping that, by the time they have to pay back the bonds, they’ll have a system of tolls in place to pay that will provide the needed revenue. And then they’ll issue permanent bonds, backed by the promise of future toll revenue and use those bonds to pay off the short term “payday” loan. But that presumes a number of things: critically, that tolls will produce enough revenue to pay back those bonds.

That’s exactly what’s happening with the I-205 Abernethy Bridge and the I-5 Rose Quarter freeway widening.

First, the Abernethy Bridge. ODOT moved ahead with this project even though it didn’t have an approved funding plan in place. It also went ahead with the project even as the construction bids came in twice as high as the program’s cost estimate ($500 million, up from $250 million in 2018). It is paying for the Abernethy Bridge in the short term by taking money that the Legislature initially earmarked for the I-5 Rose Quarter project. ODOT also plans to issue $600 million in short-term bonds. And ultimately, it hopes to repay these sources of borrowing with money it gets from selling more bonds to be paid back from future tolls. But tolling hasn’t gotten approval through the federal environmental review process–and may not–but regardless the state will have to pay off these bonds.

Second, there’s the I-5 Rose Quarter project. In 2017, the Oregon Legislature approved the project, based on ODOT’s estimate that the project would cost $450 million. The Legislature earmarked that amount in gas taxes for the Rose Quarter, but in 2021, allowed ODOT to also use this same money for the Abernethy Bridge. In the mean time, however, the cost of the Rose Quarter project doubled and then tripled: it now stands at as much as $1.45 billion. But, as noted, ODOT has diverted most of the original $450 million provided by the Legislature to the Abernethy Bridge project–so now that Rose Quarter project is perhaps a billion dollar–or more short of the money needed to pay for its construction.

Even so, it’s apparent that ODOT plans to move the project forward, even though it doesn’t have identified funds to pay for all of it. It’s planning an “Early Work” package of a few selected construction projects. It is the classic “driving stakes” strategy to get the project started, and then come back to the Legislature to ask for money to finish the job—no matter how much it ends up costing.

Ultimately, ODOT is counting on toll-backed bonds to pay for both projects. Oregon Transportation Commission Chairman Bob Van Brocklin testified in March, 2022 that all these projects hinge on toll financing. But as yet, ODOT hasn’t undertaken the detailed financial analyses that will be required to sell toll backed bonds. Both private markets and the federal government require bond issuers to commission independent “investment grade analyses” that develop realistic estimates of actual toll revenue. Without an investment grade analysis, it’s effectively impossible to know how much money in bonds the state would be able to sell to finance either of these projects.

Oregon DOT has no experience actually collecting tolls, and consequently, no real experience in projecting how much toll revenue these facilities might provide. But the financial consequences of this approach are very clear. If, and more likely, when toll revenues aren’t as much as are needed to pay for these projects, the state will be legally obligated to dip into other transportation funds (state highway funds, and under the terms of HB 3055, passed by the Legislature two years ago, federal transportation grants) to pay off bond holders before the state spends money on anything else.

If this seems like a risky and foolhardy strategy, it is because that’s exactly what it is. Unless, of course, you are a state highway agency that only cares about building more and more roads. For the manic road-builder, this is an ideal strategy: it allows you to build as much as you want today, and whether the tolls are sufficient or not, future legislatures and future taxpayers will be required to make up any shortfalls. And, as we’ve noted, in the face of the climate crisis, this approach to road finance is deeply perverse: Once the state builds more roadways, if its efforts to reduce driving (and cut carbon emissions) are successful, the toll revenue shortfall will have to be made up by cutting other transportation spending. The state will even be obligated to use federal funds (which can be used flexibly for transit, walking, and cycling projects that would reduce greenhouse gas emissions) to pay off the bond-holders who financed the under-used highway capacity.

Wholly Moses

This strategy of driving stakes (getting projects started, even before their full costs are known) and selling bonds issuing debt that legally obligates the state to finish the projects, is a classic road-building scheme. Oregon DOT’s plan to get started on several of these projects, and to finance them by short-term borrowing and bonds, backed with a legal pledge of both future toll revenues and other state and federal transportation funds, mimics the classic scam developed by America’s original highway builder/power broker, Robert Moses, in the 1930s.

Moses guided public investment in New York for decades and the city and state today still bear the deep imprint of his choices, chief among them, the decision to remake much of the region to facilitate the movement of automobiles. Part of his legacy is the toll bridges and a network of highways that slashed through urban neighborhoods—in his words—like a meat-ax. But there’s another more subtle, but equally enduring element of the Moses legacy: a pattern of practice followed to this day, in one form or another, by highway departments around the country.

Moses locked up all the revenue from publicly financed bridges and tunnels, and at a time when public transit was starved for investment, plowed it all back into a steady stream of new road capacity that demolished neighborhoods, furthered sprawl and increased car dependence. The Oregon Department of Transportation seems determined to take a page out of the Moses playbook.

To see how these two patented Moses gimmicks work, we turn the microphone over to his biographer, Robert Caro.

Driving Stakes

The key techniques are two-fold: First, just getting projects started. Several of these projects (the I-5 Bridge replacement, and the I-5 Boone Bridge), haven’t even completed their planning, so their full costs are unknown. The second technique is to issue bonds to pay for the project, secured by toll revenues.

Early on, Moses learned the value of starting construction of a highway—driving stakes in the ground—even if he didn’t have all the financing in place, and regardless of whether he knew (or honestly revealed) the actual total cost of the project. Just getting something started made it almost impossible for legislators or other officials to deny him whatever resources he needed to finish the project. Caro writes:

Once you did something physically, it was very hard for even a judge to undo it. If judges, who had to submit themselves to the decision of the electorate only infrequently, were thus hogtied by the physical beginning of a project, how much more so would be public officials who had to stand for re-election year by year? . . . once you physically began a project, there would always be some way found of obtaining the money to complete it. “Once you sink that first stake,” he would often say, “they’ll never make you pull it up.”

And this tactic turned minimizing or hiding the true cost of a project into an indispensable means of getting things moving:

Misleading and underestimating, in fact, might be the only way to get a project started. . . . Once they had authorized that small initial expenditure and you had spent it, they would not be able to avoid giving you the rest when you asked for it. . . . Once a Legislature gave you money to start a project, it would be virtually forced to give you the money to finish it. The stakes you drove should be thin-pointed—wedge-shaped, in fact on the end. Once you got the end of the wedge for a project into the public treasury, it would be easy to hammer in the rest. (Caro at 218-219)

Selling Bonds

One of Moses’ key insights was that municipal revenue bonds worked like an alternative, overriding form of government authority, in his case, overriding future legislative control or second thoughts. The contract between bond issuers (like a state agency) and bond buyers can’t be impaired by future legislative changes. A promise to dedicate certain revenues to an agency in a bond indenture can tie them up for years or decades, or as Moses showed, forever. Bonds, once issued, become a virtually unbreakable contract. Once ODOT sells bonds backed by the pledges of toll revenue (and other federal and state transportation revenues) the state is permanently, and preemptively committed to giving it all the toll revenue (and in the case of HB 3065, forfeiting other revenue to make up any shortfall).

Caro explains the original structure Moses crafted when he drafted amendments to New York statutes governing bonds issued by his Triborough Bridge Authority.

Legislation can be amended or repealed. If legislators were in some future year to come to feel that they had been deceived into granting Robert Moses wider powers than they hand intended—the right to keep tolls on a bridge even after the bridge was paid for, for example—they would simply revoke those powers. But a contract cannot be amended or repealed by anyone except the parties to it. Its obligations could not be impaired by anyone—not even the governing legislature of a sovereign state. Section Nine, Paragraphs 2 and 4, Clauses a through i, gave Robert Moses the right to embody in Triborough’s bonds all the powers he had been given in the legislation creating Triborough. Therefore, from the moment the bonds were sold (thereby putting into effect the contract they represented) , the powers he had been given in the legislation could be revoked only by the mutual consent of both Moses and the bondholders. They could not be revoked by the Authority or by the City whose mere instrumentality he was supposed to be.

(Caro, at 629-630)

The combination of these two strategies—driving stakes and selling bonds—is enough to lock the state into an expensive and environmentally destructive freeway building spree. And once the bill passes, and the bonds are sold, future legislatures will find themselves as powerless to rein in ODOT as New York was to stop the Moses meat ax from hacking through New York City.