Later this month, the Federal Reserve Board (or “the Fed,” as it’s often referred to) will raise interest rates. After seven years of very loose monetary policy designed to facilitate economic recovery from the Great Recession, the Fed now apparently thinks that the economy is healthy enough to stand higher interest rates.

Clearly, the financial markets will be paying rapt attention; in fact, guessing the date of the rate increase has been the principal occupation of Fed watchers for two years. But beyond the headlines, should cities care?

Yes. To begin with, there are some direct impacts on city finances. Municipal governments are big borrowers, especially for things like public works, and if the Fed’s rate rise pushes up interest rates, then that means it will be more expensive for cities to borrow to fund those projects.

But cities should also be concerned about the effect on national economic growth. While the recovery from the Great Recession has been a long, slow slog, cities in particular have seen steady economic growth for the past several years.

Arguably, housing is the sector of the economy most sensitive to changing interest rates. Low interest rates make housing investments more attractive, and the one bright spot in a still deeply depressed housing market—multifamily construction in cities—has depended heavily on the Fed’s extended period of low rates. Multifamily starts have fully recovered to their pre-recession levels, while single family starts have languished at near historic lows. As we’ve noted, the trend toward apartment construction is attributable to a number of factors: a growing demand for urban living; poor credit availability (and creditworthiness) among young adults who have traditionally purchased entry homes; strong rent growth; plus relatively attractive interest rates for the kinds of institutional and large-scale investors who finance apartment construction.

While many of these factors aren’t going anywhere, rising interest rates may determine whether some apartment construction projects go forward. A significant rise in long term interest rates could mean that some apartment projects don’t pencil out. Thirty year mortgages are currently running about 3.72 percent.

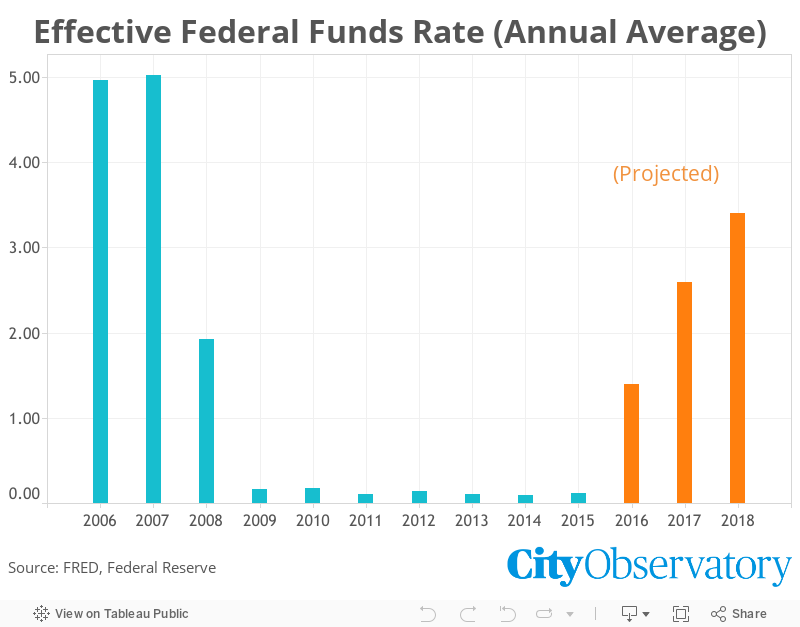

The big question for the housing market is whether long term rates increase. Fed policies chiefly affect short-term rates, and the link between long-term and short-term rates is indirect and variable. The Federal Reserve’s main policy lever is the federal funds rate, which plays a key role in determining short term interest rates, but which affects longer term interest rates, like mortgages with, as the economists are wont to say “with long and variable lags.” The Fed uses its financial transactions, including the rates it charges to banks, and its purchases of securities, to target a particular short-term interest rate. That, in turn, influences other interest rates in the economy. Back in 2008 and 2009, the Fed successively reduced short term interest rates to almost zero to help support the economy during the Great Recession. A majority of the Federal Reserve Board of Governors seems to think that they should “normalize” their policy and raise rates.

This is what “highly accommodative monetary policy” looks like. It is coming to an end.

In June, Zillow economists projected that Fed tightening via short term interest rates would push up mortgage rates. Assuming a constant spread between short and long term rates, they estimated that rates on 30-year fixed mortgages would rise from rise from 3.84 percent in May 2015 to 4.63 percent by December 2015, 5.63 percent by December 2016, 6.88 percent by December 2017, and 7.75 percent by December 2018. Some economists seem to think that short-term rate increases will have little impact on long term rates—in economists’ parlance, the yield curve will flatten. They think that economic growth is sufficiently well-established that long term rates will rise very little.

While the immediate effect on cities may well be seen in the housing sector, the larger concern has to be the state of the macroeconomy. If overall job growth (which has been running at about two percent annually) falls off, it makes nearly all of the economic challenges facing cities worse. Falling job growth would likely lead to higher rates of unemployment, weaker wage growth, and lower tax collections. Many economists think the Fed tightening is premature, that the economy is not fully recovered, and that there are significant downside risks to raising rates now. One former Fed Economist argued that the economy is still operating well below potential, and can expand further with little fear of inflation. Others note that the recent appreciation of the U.S. dollar can be expected to be a drag on U.S. economic growth, and that an interest rate hike would add add to this drag.

At City Observatory, we generally focus our analysis on cities and metropolitan economies, and look at economic trends as they play out in particular geographies. But occasionally, it’s important to step back at consider the broader national macroeconomic context. City and metro economies each have their own dynamics, but ultimately find their options shaped by trends in the national economy. This is one of those times.

It’s become increasingly popular to assert that cities can replace federal policy activism to tackle many national and global problems. And while we take a backseat to no one in stressing the importance of cities, in some cases, if the national government gets key policies wrong, it can be almost impossible for cities to make progress. If timidity about potential inflation prompts the Fed to engineer a rate rise that slows economic growth—or pushes us into a recession—much of the progress that cities have made in growing jobs and expanding opportunity will be at risk. In the months ahead, keep a close eye on multifamily housing starts and the job growth rate to see whether the Fed got it right—or not.