A new report from the DC Policy Center shows the inner-workings of the shadow rental market that is a key to housing affordability

Too often, our debates about housing policy are shaped by inaccurate pictures of how the housing market really works. A new report from the D.C. Policy Center provides a remarkably clear and detailed picture of the rental marketplace. And its richer and more complicated than accounted for in the usual oral tradition of housing markets.

The “shadow” market for rental housing. We generally assume that that there are two types of housing, rental and ownership. Rentals tend to be multi-family apartment buildings, single-family homes are owner-occupied. Rentals stay rentals;owner-occupied homes state owner-occupied, and never the twain shall meet. Except that lots of single-family homes do get rented; and some of them, even though once rented, get sold and occupied by a new buyer. This fluid movement of homes in and out of the rental market is seldom mentioned in housing policy. Taylor calls this the “shadow” market for housing.

The report makes two facts clear about the shadow housing market. First, its a considerable part of the District’s rental housing stock. Using detailed administrative data, Taylor calculates that there are more than 60,000 single family homes, condominiums, flats and other small scale rentals which represent about a third of the District’s rental housing. Importantly, many of these units are in high opportunity neighborhoods, so if you’re a renter, and you’re looking to get a better environment for your kids, the “shadow” market may be the way you access such neighborhoods.

The other fact is that housing regularly moves in and out of the shadow market. Again, by laboriously constructing a longitudinal picture of the occupancy of individual houses–something that’s simply not available in most housing statistics–Taylor computes the share of the “shadow” housing that was rented in 2006 that is owner occupied today, also the share of the shadow housing we have today was owner-occupied in 2006.

Homeowners frequently move their units in and out of the rental market. One fifth of the 87,000 owner-occupied condominiums and single-family homes in 2006 had become rentals in 2019. Conversely, of the 39,500 condominiums and single-family homes that were rentals in 2006, nearly 15,000 (38 percent) were, as of September 2019, owner-occupied

Housing can and does move between these categories, in response to the incentives that owners have to rent housing versus selling it.

These two fundamentals shed a new light on how we think about rent control. If you view the number of housing units in the rental market place as fixed (mostly big apartment buildings, owned by corporations or real estate trusts), its hard to imagine that the housing will be withdrawn from the rental market and occupied by its owners. But that doesn’t hold for our shadow housing. If renting out a single family home or condominium no longer seems like a viable or profitable proposition, the owner has lots of choices. She (or someone from her extended family) can move into the house, or she can put it up for sale.

If you read the report carefully, you will see it puts the lie to one of the most pernicious and misleading terms in housing policy “naturally occurring affordable housing.” The assumption that a lot of people have is that as housing ages it automatically must decline in price, and become more affordable. That’s only true if there’s an adequate supply of housing in the face of market demand. If–as is the case in Washington–its hard to build new units, and there are lots of prospective renters who can pay top dollar, its highly likely that investors will fix up existing units rather than allow them to decline in quality (and rent). As Brookings economist Jenny Schuetz explained at the Atlantic earlier this year, its entirely possible for housing to “filter up,” reducing the supply of affordable housing.

Taylor’s report provides additional nuance for understanding how this process unfolds. Owners of shadow market rental homes and condos have choices about whether and how much to invest in upkeep, and what price point to seek in the rental market. They (and their extended family) are also potential occupants of the homes they own. And depending on the market, they can rent out their home as is, fix it up, occupy themselves, or sell it to another owner occupant. The key point is that there’s nothing “natural” about the process by which an individual home becomes affordable (if it does). It’s all about the policy environment and the incentives.

All this is extremely salient to discussions about tightening rent control in the District of Columbia. The District has had a modest form of rent control since the 1980s, restricting rent increases to the cost of living plus 2 percent, but with provisions to allow rent increases when apartments are vacant and when they’re rehabilitated. And the rent control doesn’t apply to newly built apartments. But there are moves afoot to reduce the allowable rent increase to just the cost of living, and to fix rents even when units become vacant.

Taylor’s report suggests that the policies could have a dramatic effect on the decisions of the shadow rental market owners. By reducing the economic returns to renting, rent control is likely to prompt many owners to take their units out of the rental market place, occupying them themselves, or selling them to new owner occupants. And importantly, rent control is likely to stem the flow of other units into the shadow market. As Taylor’s work shows, there’s currently a regular influx of existing homes from ownership into rental status: If that dries up, the city’s rental housing supply will shrink.

The conventional criticism of rent control is that it discourages the construction of new apartment buildings. But this report makes it clear that the effects on housing supply are more subtle and pervasive. Because of the fluidity of the shadow market, rent control can have a negative effect on the rental housing supply because it encourages some owners to take currently rented units out of the market, and also because it is likely to discourage others from entering the rental market.

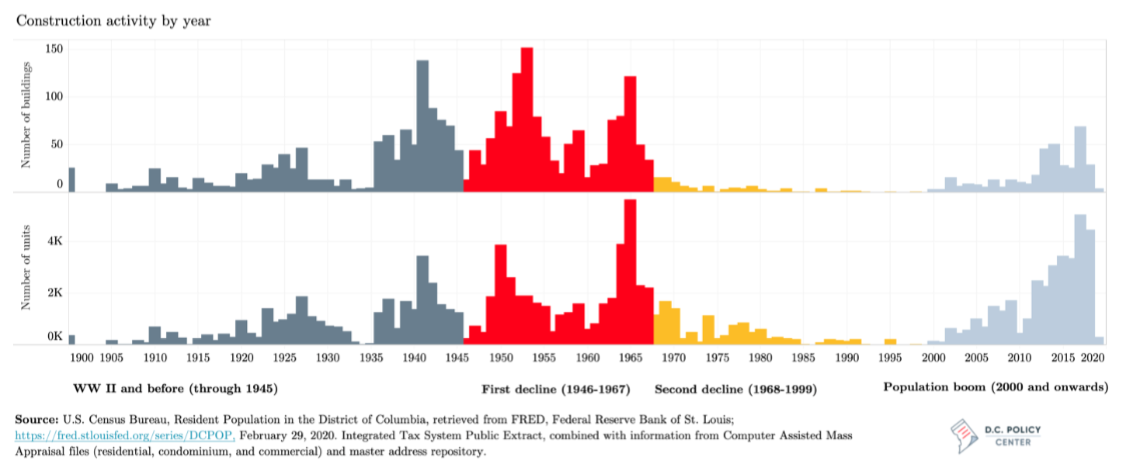

The report provides, in passing, evidence for one other feature of the housing market that’s often overlooked. Most multi-family housing in cities gets built in spurts, in booms, and in between booms, very little is built. In DC there was a surge in housing construction in the twenties (grey), and again just before and after World War II, and then a decades long drought from 1950 through the turn of the century. Only in the past decade has another housing construction boom occurred. The dearth of housing built from 1960 through 2000 is why the District has a shortage of “naturally occurring” affordable housing (and the bust is a good indication of why that term is so misleading).

While in the height of a boom, it seems like building may go on forever, that’s seldom the case. It takes a unique constellation of factors (a robust local economy, low interest rates, banks and developers willing to take a risk), which may be short lived. The message to cities is that you have to make sure housing gets built in boom times, or it may not be built at all.

As an alternative to more stringent rent control, Taylor outlines a proposal for “inclusionary conversions” that would negotiate contracts with owners of existing rental units to maintain them at affordable rents. The District would make payments to owners, who would be contractually obligated to provide below market rental units. The concept would help preserve the existing rental housing stock for low and moderate income households, and rather than imposing all of the costs on landlords, would spread them more broadly to the public, through tax abatements.

Finally, Taylor emphasizes a point that we thing is important to communities everywhere. We increasingly expect small scale landlords to play an important role in providing additional housing in cities, through liberalization of “missing middle” housing like duplexes, triplexes, fourplexes, and accessory dwelling units. But all these measures assume that we have willing investors and that being a landlord is a viable proposition, As Taylor writes:

. . . a substantive part of the District’s rental housing is dependent upon the willingness on the part of smaller landlords to keep their units in the rental market. Further, some of the policies the city is pursuing to increase housing supply (such as Accessory Dwelling Units or infill development) relies on convincing current homeowners to become landlords. The District’s rental housing policies, however, are generally focused on large rental apartments, and do not consider the constraints for and the capacity of smaller landlords in obtaining financing, meeting regulatory requirements, and working within the requirements of tenants’ rights laws. A broader rental housing policy that recognizes the importance of these smaller landlords in expanding the city’s housing supply would be a step in the right direction for the District of Columbia

If we’re really interested in promoting additional housing supply, and assuring a wide range of rental options in neighborhoods throughout our cities, we should be paying much more attention to the size and fluidity of the “shadow” rental market. This report shines a useful light on its crucial role, and is something every city should look to duplicate.

Yesim Sayin Taylor, Appraising the District’s rentals

The role of rental housing in creating affordability and inclusivity in the District of

Columbia, (Washington: D.C. Policy Center, 2020)