The big economic news of the past month was the Federal Reserve Board’s decision to begin raising interest rates after years of leaving them at near-zero levels. The first increase in the short-term interest rate the Fed charges banks will be one-quarter of one percent, but there’s an expectation that the Fed will continue to raise rates through the remainder of the year.

Shadow boxing at the Fed

The theory behind the Fed’s policy is that rate hikes are needed to normalize financial markets—it’s unusual for interest rates to hover near zero for so long—and to fend off the prospect of inflation. The Fed raises interest rates when it fears that inflation might be getting out of hand, and it wants to tamp it back down.

As we’ve argued before, this move isn’t doing cities any favors, as it’s likely to hold back economic growth before urban areas, like the rest of the country, have returned to the growth path they were on prior to the Great Recession. The timing and wisdom of this rate increase is very much in question. Never mind that there’s virtually no evidence of inflationary pressure in the economy today, nor has there been for decades. Many of the Fed’s officials came of professional age in the seventies, when inflation was a real concern, and like so many aging generals, they are still re-fighting the last war. As The Economist’s Ryan Avent observes, the economy has changed a lot since then, what with technology, globalization, the decline of unions, and a steady attenuation of wage and price expectations, but “The Fed seems not to realize that it is risking America’s recovery out of fear of an inflationary dynamic that it ruthlessly and utterly eliminated three decades ago.”

So what are the portents of inflation that worry the Fed? For most workers, wage increases have been negligible. Health care costs are subdued. Although macroeconomists generally discount food and fuel prices on account of their short-term volatility, sustained reduction in energy prices (i.e. oil costing something closer to $30 a barrel for a year or more, rather than the roughly $100 a barrel it has averaged for the past few years) can’t be erased from the inflation numbers.

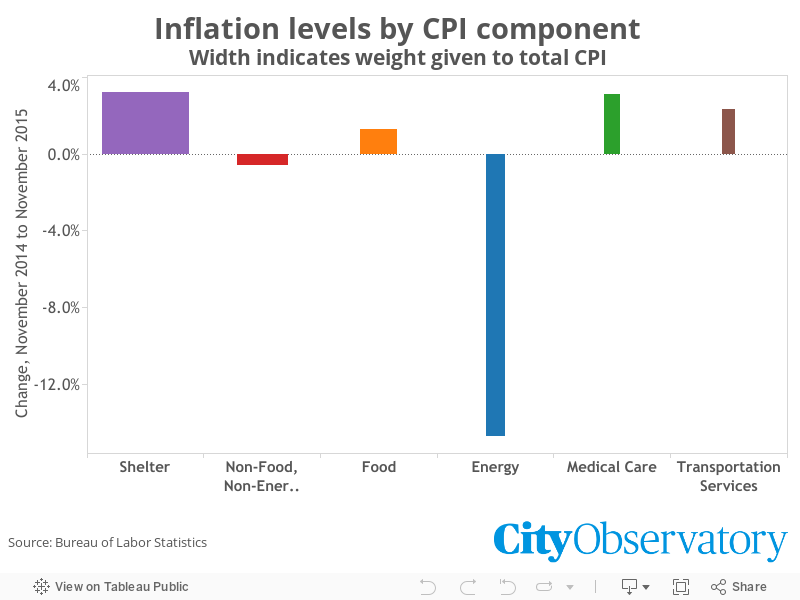

As the Wall Street Journal’s Ben Leubsdorf points out, the only segment of the economy that’s exhibiting significant price increases is rental housing. But because shelter makes up a third of the consumer price index, the growth of housing prices is hiding weak growth in virtually all other sectors. In fact, if you exclude rents from the consumer price index, price levels are decreasing, not increasing. In other words, the Fed is taking steps to fight inflation when much of the economy is experiencing deflation.

The measure of rent in the consumer price index includes both the payments by renters, and an allowance for an equivalent cost for homeowners.* Over the past twelve months, rent is up 3.2 percent, faster than any other component of the consumer price index. In that same time, thanks to declining energy prices, the overall index is up only 0.5 percent.

Can the fed deal with rents directly?

The fact that rising rents are the chief contributor to price increases in the macro economy implies that the Fed’s monetary policy is problematic for a couple of reasons:

First, if, outside of housing, prices are falling, that suggests that it is premature for the Fed to raise interest rates. If the economy is in a deflationary condition, raising rates is likely to cut growth and possibly even drive the economy into recession. The turmoil in global financial markets in the past few weeks is evidence that many investors are uneasy about the health of the worldwide economy.

But second, if rising rents are the underlying inflation threat, then a very different policy response is called for. As we’ve noted at City Observatory, the reason for the big run up in rents has a lot to do with the nation’s shortage of cities, and of the shortage of multi-family rental housing, especially in walkable urban neighborhoods.. While there’s been a resurgence of construction of this kind of housing, in general, the supply response hasn’t been big enough, or fast enough, to blunt the rise in rents.

And here’s the interesting point: the Fed’s policies play a critical role in housing finance. The principal channel through which monetary policy works is by influencing economic activity in interest rate sectors of the economy. The way the Fed fought inflation in the sixties, seventies and eighties was by jacking up interest rates, choking off the flow of credit to the housing sector, and cooling off the economy. As Economist Ed Leamer summarized it provocatively: “housing is the business cycle.”

Interest rates for construction loans and for commercial real estate purchases strongly influence the feasibility of new investment in rental housing. If interest rates on these loans rise, fewer new apartments will get built, demand will continue to outstrip supply, and rents will likely be pushed up further. If the Fed is worried about inflation, maybe it needs to make sure we keep building more apartments.

A Modest Proposal

All this suggests that if the Fed takes its inflation-fighting mandate seriously, it might want to consider a sectorally targeted policy for multi-family housing. For example, if the Fed were to shift some of its purchases of securities to include a greater share of construction loans and mortgages on multifamily rental property, it could hold down growth in interest rates (or even drive rates down) in this sector, which would encourage more construction—adding to supply and helping to address inflation in the one sector where it seems to be a problem. And while the Fed seems concerned that its easy money policy may be prompting bubbles in other sectors, rising rents are a sign that more investment is needed in this sector to forestall the kind of supply constraints that fuel inflation.

The Fed is generally keen to deflect responsibility to Congress and the President for addressing what are referred to as “structural” problems in the economy. In general, the Federal Reserve also eschews sectoral interventions in the economy. But it’s not unprecedented. During the financial crisis in 2008, the Fed was instrumental in creating a number of special purpose financial facilities to help assure the liquidity of the banking industry—out of a concern that a structural implosion in this structure would cause serious damage the entire economy. To promote the economic recovery, the Fed later engaged in a program of “quantitative easing” buying up long term government bonds—and mortgage backed securities—to help hold down long term interest rates and buoy investment.

Of course, finance isn’t the only policy of importance here: cities have to zone land for apartments. But absent the ready availability of financing, new apartments won’t get built. And if long-term rates rise, that’s likely to reduce the number of new projects that go forward. So far, at least, mortgage rates have remained stable in spite of the first step in the Fed’s “normalization” process. But stay tuned.

Late last year, Jason Furman, the Chair of the White House Council of Economic Advisers gave a major speech connecting the dots between local zoning and problems of housing affordability and inequality. The critical—but largely unnoticed role that rising rents are playing in inflation is another indicator of the growing economic importance of what happens in cities. So perhaps it’s time for Janet Yellen and her colleagues at the Fed to take a closer look at what’s happening in the nation’s cities as they set monetary policy.

* Technical note: The shelter component of the consumer price index measures the increase in housing costs based on the current cost of occupancy. For renting households, this includes their rent. For homeowners, the Bureau of Labor Statistics calculates “owners equivalent rent”—the amount that homeowners would have to pay if they rented their homes, rather than owned them. Changes in the amount of this “imputed rent” are used to figure inflation in housing costs.