At City Observatory, we love fat reports full of data, especially when they shed light on important urban policy issues. Last week, we got the latest installment in a long-running series of annual reports on housing produced by Harvard’s Joint Center on Housing Studies (JCHS). The State of the Nation’s Housing, 2016—aka SONH2016—presents copious details on the housing situation. This year, it particularly highlights the growing problem of housing affordability. (We summarized last year’s report here.)

There’s a lot to digest in this report. Our review focuses on four big issues, how the report describes affordability, its analysis of recent developments in the housing market, the outlook for homeownership as a wealth building strategy, and the implications of all this for housing policy.

Housing Affordability

SONH2016’s headline finding is the growing number of households spending half or more of their income on housing. Using the 30 percent of income standard, the report estimates the number of rental households with affordability problems has increased by 3.6 million since 2008. The report continues to use the 30 percent of income standard even though there are real questions as to whether it really reflects affordability, or addresses the housing/transportation cost tradeoff. And the number of households spending 50 percent or more of their income on rent has increased by 21 million to 11.4 million over that same time period (p. 4).

We agree that housing affordability is a widespread and serious problem. But what seems lacking from SONH2016 is a thorough diagnosis of the causes of the affordability problem and an appropriately scaled set of solutions. There’s passing reference to local land use controls as a contributing factor to the problem of housing affordability: “High rents reflect several market conditions, including a limited supply of land zoned for multifamily use and a complex approval process that adds to development costs.” (p. 4) But the report emphasizes the impact of land use controls on building affordable housing, and aside from this brief mention, offers little comment—and no policy recommendations—about how to ameliorate the effects of supply constraints by changing local zoning.

While SONH2016 does a thorough job of amassing statistics that chronicle the growth and extent of affordability issues, it spends relatively little time describing policy actions that might make a dent in the problem. On the last full page of the report, the authors offer their outlook on housing challenges. The note that only modest additional resources have been made available to support low income housing construction —we’re told (p. 36) the biggest program in the past decade is the recent authorization of the $174 million Housing Trust Fund (which works out to about $16 for each of the 11 million households spending 50 percent or more of their income on housing). In effect, we’re presented with a daunting problem without any commensurate solution.

The Housing Market

The report tries to sound some optimistic notes about about single-family homeownership. But they come off as weak reeds in the face of what continues to be a highly depressed sector of the economy. The report highlights an increase in single family housing construction (p. 1: “new home construction was up by a healthy 11 percent”) but later concedes that the total number of homeowners, and the homeownership rate, has continued to fall (p. 16).

On the plus side, the report helps dispel a commonly reported misperception about the growth of McMansions. The data show that though large homes (greater than 3,000 square feet) have become a bigger share of the market, that has more to do with the utter collapse of the market for small homes than it does with any expansion of the appetite for large ones. In fact, McMansion-sized homes are still being built at just half the rate of a decade ago (200,000 units per year compared to 400,000 at the peak). (See p. 8). As we’ve explained at City Observatory, the “McMansion/Multi-Millionaire” ratio has actually been falling.

Very much to its credit, SONH2016 calls out the growing economic segregation of US housing. It says that poverty in the US has become more concentrated, and bluntly calls out the location of public housing and exclusionary local zoning as major causes of this problem (p. 35).

Homeownership, Wealth and Home Prices

State of the Nation’s Housing continues to promote homeownership as a reliable wealth-creating strategy, what it calls “the wealth building potential of sustained home ownership” (p. 21) The report cites data for the net wealth gains of homeowners who managed to hang on to their homes, but combines data from those who bought over the entire decade (1999 to 2009), which conceals the key fact that those who bought in say 2001 or 2002 had a very different experience than those who bought at the height of the bubble. The report omits the fact that homeowners collectively lost something on the order of $7 trillion in the housing bubble, and that these losses fell disproportionately on low income and minority households. And, as Calculated Risk’s Bill McBride points out, a decade after the peak of the housing bubble, real, inflation-adjusted home prices are still 17 percent below their peak.

This series of State of the Nation’s Housing reports have been been issued for nearly three decades. Over the years, there have been a number of recurring themes. Concerns about housing affordability have been hardy perennials. A decade ago, concerns about affordability were also in the report’s headlines, although for very different reasons. The 2006 State of the Nation’s Housing dealt primarily with how rising home prices were reducing affordability for homebuyers. (This particular aspect of the affordability problem was corrected by the popping of the housing bubble, something that that year’s SONH didn’t forsee.)

In 2006, with the nation’s housing bubble about to burst, it offered confident reassurance: “large house price declines seem unlikely for now . . . the long term outlook for housing is bright . . . STRONG DEMAND FUNDAMENTALS . . . with each generation exceeding the income and wealth of its predecessor, growth in expenditures on home building and remodeling should match if not surpass the current pace . . . (State of the Nation’s Housing 2006, page 2). Now, nearly a decade later, the housing sector’s contribution to GDP remains fully one-third lower than its historic average (SONH 16, Figure 12).

The point here isn’t that so much the SONH made a bad forecast, but more than it gave bad advice. Far from being a reliable source of wealth generation, housing was a very risky proposition that was about to impose huge costs of millions of households. Prior to 2007, one might argue that a 20 or 30 percent drop in home prices was improbable. But in light of the human and personal costs of the last housing bubble, it seems like the report ought to be a bit more cautious in its approach to the question of whether, for whom and under what circumstances home ownership is a good investment.

Federal Housing Policy

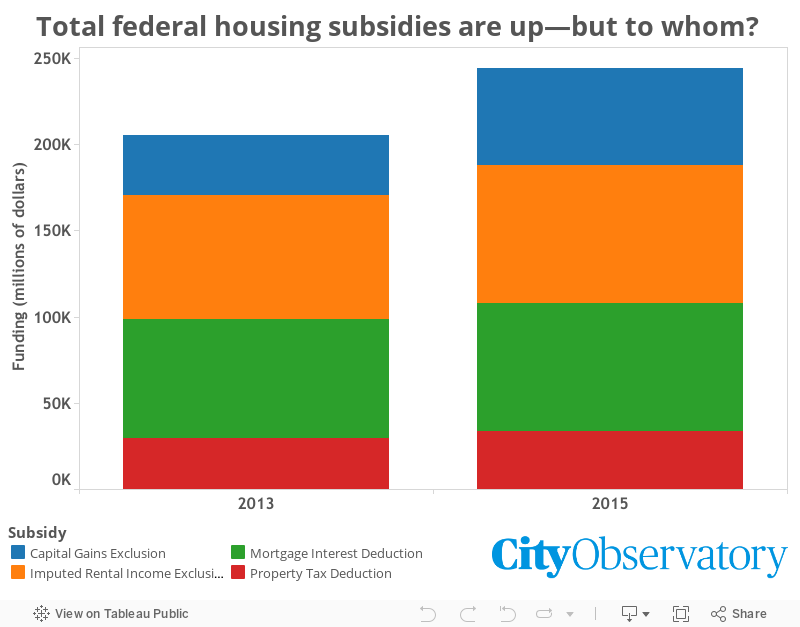

There are some surprising omissions from the report. You’ll find no mention of the biggest and most expensive federal housing subsidy programs: the favorable tax treatment of owner-occupied housing, in the form of the mortgage interest deduction, the exclusion of imputed rental income and favorable treatment of capital gains on housing. Collectively, these policies amount to a $250 billion annual subsidy for homeownership, which thanks to a falling homeownership rate, is going to a smaller fraction of American households each year.

It’s also interesting to note that at a time when SONH16 frets that our nation’s housing problems are being aggravated by “dwindling federal subsidies” (p. 31), that federal resources for housing are “dwindling” (page 31), the value of the federal tax subsidies has increased sharply. According to the Congressional Budget Office, the combined value of favorable tax treatment for owner occupied housing increased by $39 billion between fiscal years 2013 and 2015.

If we’re really concerned about housing affordability, we have to do more than periodically trumpet alarming statistics. We really ought to plainly identify root causes, and spell out the public policy choices that we’ve made — through local zoning and public subsidies — and talk about the scale of the effort required to materially change the situation.

A casual reader of the SONH16 may come away with the impression that federal housing policies are ineffectual and under-funded, but that’s hardly the case. We have a well-funded federal housing policy that works quite well—if you agree that its intended purpose is to provide generous support, particularly for the wealthiest households, to own their own homes. In our view, a more comprehensive framing of federal housing policy–one that encompasses tax subsidies to homeownership–provides a much more useful context to understanding our housing problems and formulating commensurate solutions.

If you’re interested in housing, particularly the tale of the tape when it comes to a wide range of housing statistics, SONH 16 is an invaluable resource. But when it comes to thinking about housing policy, and specifically, identifying the root causes of our affordability problem and the nature and scale of the policy solutions that would need to be undertaken to actually move the needle on the indicators presented here, you’ll have to look elsewhere.