What to make of the high credit scores of new renters in some markets: alarm bell or success signal?

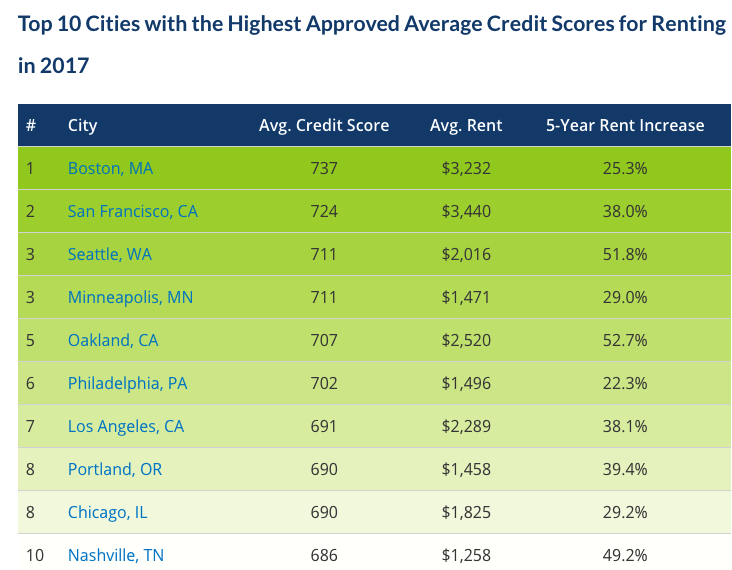

RentCafe–one arm of Yardi Matrix, a real estate data and services firm–has a very interesting new data series on the credit scores of successful and unsuccessful apartment seekers in different cities. Rent Cafe runs a tenant screening service on behalf of landlords, and a key variable that they report to their clients is a household’s credit score (which ranges from a low of 300 to a high of 800). Rent Cafe’s research has shown a strong correlation between a strong credit score and a high probability of having your rental application approved. Nationally, if you have a credit score over 750, your chances are 98%, if it’s between 500 and 600, then you have only about an 67% chance of getting the apartment.

In some markets–like Boston, San Francisco and Seattle–successful rental applicants have sterling credit. In these top cities, new renters have credit scores over 700.

To Rent Cafe, the high scores in these cities are a kind of alarm bell. You apparently need really great credit to rent an apartment in these places.

What Credit Score Do You Need to Rent an Apartment? Insanely High, If You’re in Boston or San Francisco

But there’s another possible view: it’s likely that high credit scores signal just how robust the local economies are in these communities, and furthermore, how much households with strong credit are choosing to rent rather than to buy. Given that most of these communities have very expensive home prices, it may be that many credit-worthy households who might otherwise prefer to buy a home end up renting. And because Rent Cafe is reporting the average credit score, the average renter in these cities just has better credit.

Conversely, in some other cities, if you have a high credit score, you may find it more affordable to purchase a home rather than renting. This selection effect would explain why renters have much higher average credit scores in high-priced markets than in low-priced markets.

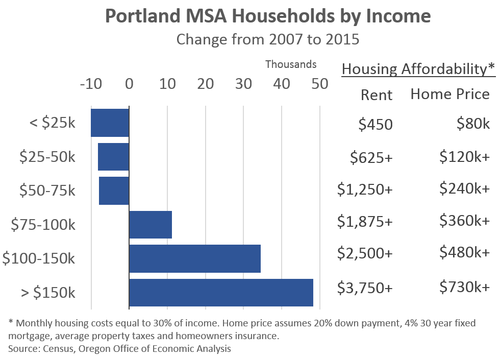

It’s also likely that credit scores are rising because the personal financial situation of the typical renter is getting better. Rent Cafe notes that the credit score of the typical approved applicant has increased about 12 points in the past three years, from 638 in 2014 to 650 this year. This is consistent with other evidence showing steady income gains in most metro economies. We’ve reported on national data at City Observatory. Oregon economist Josh Lehner has a series showing income gains for the Portland area (which ranks 8th in Rent Cafe’s list of metros with the highest credit scores for renters). Rising incomes are making housing more affordable.

Clearly, the rental market is very competitive in places like Boston and San Francisco, meaning landlords can pick and choose among tenants with a strong financial background; but the very strong credit scores of successful rental applicants in these cities is as much an indication of strong local economies (and prosperous tenants) as it is of the choosiness of local landlords. In the long run, the growing average creditworthiness of tenants may reflect the limited opportunities for homeownership in these increasingly expensive markets, where households with sterling credit who would be buyers almost anywhere else, find themselves renting instead. A new report issued by the Philadelphia Federal Reserve Bank shows a continued decline in the number of first-time home buyers nationally, a trend consistent with rising average credit scores among renters.

You’l want to take a look at the full report. The RentCafe report has detailed information on average credit scores of successful and unsuccessful apartment seekers in 100 of the nation’s largest cities. As we’ve noted, the data are drawn from RentCafe’s own client work, and so may be influenced by how complete and representative a sample of properties it covers in each market.