Hot on the heels of claims that Millennials are buying houses come stories asserting that Millennials are suddenly big car buyers. We pointed out the flaws in the home-buying story earlier this month, and now let’s take a look at the car market.

The Chicago Tribune offered up a feature presenting “The Four Reasons Millennials are buying cars in big numbers,” assuring us that millennials just “got a late start” in car ownership, but are now getting credit cards, starting families and trooping into auto dealerships “just like previous generations.”

Similar stories have appeared elsewhere. The Portland Oregonian chimed in: “Millennials are becoming car owners after all.”

Not quite a year ago, we addressed similar claims purporting to show that Millennials were becoming just as likely to buy cars as previous generations. Actually, it turns out that on a per-person basis, Millennials are about 29 percent less likely than those in Gen X to purchase a car.

We pointed out that several of these stories rested on comparing different sized birth year cohorts (a 17-year group of so-called Gen Y with an 11-year group of so-called Gen X). After applying the highly sophisticated statistical technique known as “long division” to estimate the number of cars purchased per 1,000 persons in each generation, we showed that Gen Y was about 29 percent less likely than Gen X to purchase a car.

More generally though, we know that there’s a relationship between age and car-buying. Thirty-five-year-olds are much more likely to own and buy cars than 20-year-olds. So as Millennials age out of their teen years and age into their thirties, it’s hardly surprising that the number of Millennials who are car owners increases. But the real question—as we pointed out with housing—is whether Millennials are buying as many cars as did previous generations.

The answer is no.

Auto industry analysts at the National Automobile Dealer’s Association—who have a very strong stake in the outcome—are pretty glum about sales prospects of the Millennial generation. NADA’s economist Steven Szakaly predicts it will take four Millennials to equal the sales impact of a single Boomer. This is due to a combination of factors, including Millennials’ weaker income and job prospects, and lower propensity to drive and own cars. Its also the case that waiting longer to buy one’s first car means that one is likely to own fewer cars over a lifetime, and as with housing there’s no evidence that young adults are catching up to previous generations as they age.

As we said last year, the real gold standard for intergenerational comparisons would be to look at the rate of car ownership for different generations when they were at the same point in their life-cycle, i.e., look at the car buying habits of Boomers when they were in late twenties and early thirties (during the seventies and eighties), and compare them with the habits of Gen X (25-34 in the nineties) and Millennials (25-34 from 2005 onward). Alas, we don’t have that data.

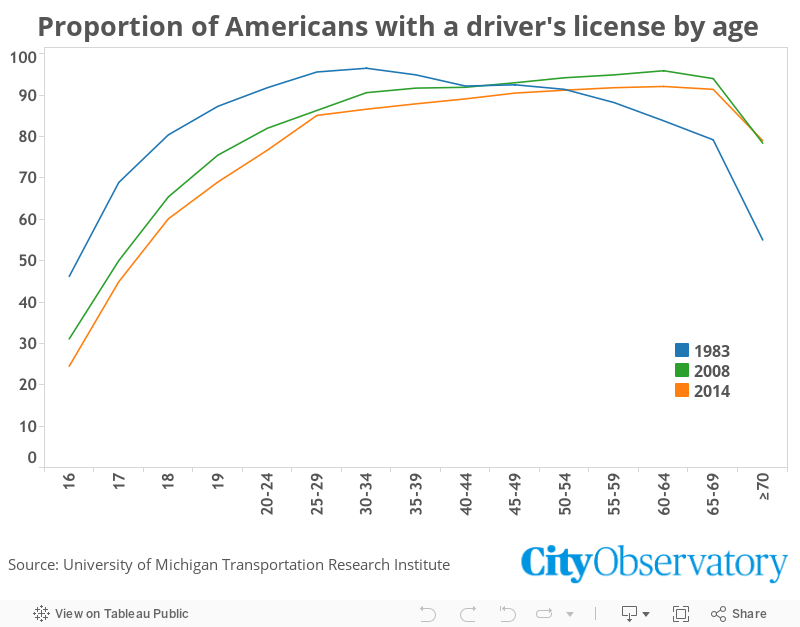

But we do have another indicator: the fraction of young adults who have drivers licenses.

Michael Sivak and Brandon Schoettle at the University of Michigan’s Transportation Research Institute analyzed US DOT data, and found big declines in the rate at which young adults get driver’s licenses. At every age up to 50 years old, a smaller fraction of U.S. adults is getting a driver’s license than a few decades ago. Today, only about 60 percent of 18-year-olds have a licence, compared with about 80 percent in the 1980s. Even among those in their late twenties and early thirties the licensing rate is down 10 or more percentage points from earlier decades. And the declines appear to be persisting and continuing as time goes on: Between 2008 and 2014, the rate of licensing declined from 82.0 percent to 76.7 percent among 20 to 25-year-olds.

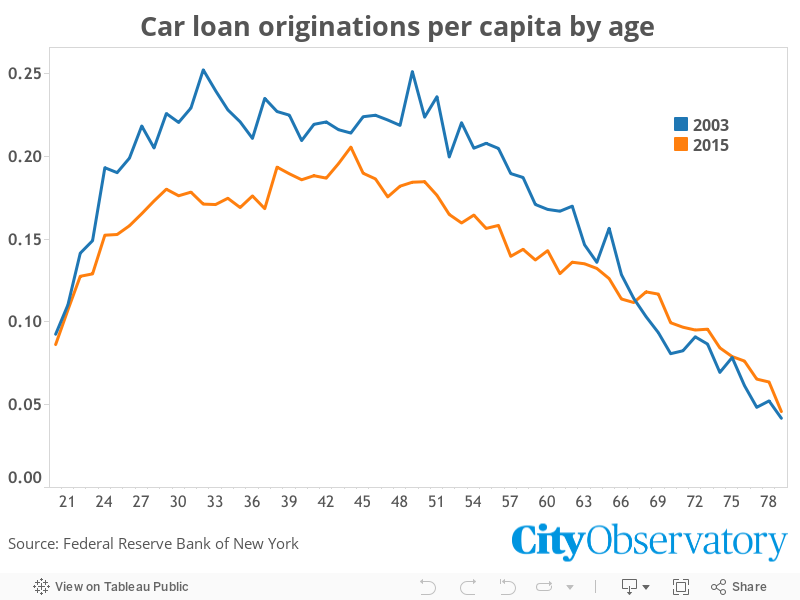

Another bit of evidence comes from financial markets. The Federal Reserve Bank of New York studied credit records to determine what fraction of persons in each age group took out an auto loan. While the total volume of automobile lending declined sharply between 2003 and 2015, the decline was most pronounced among younger age groups. Lenders made about 25 auto loans per 100 persons in their mid thirties in 2003, but only about 17 loans per 100 the same age cohort in 2015. Only those 65 or older are more likely to take out a car loan today than in 2003.

When it comes to America’s much storied romance with the car, it’s apparent that ardor has cooled, especially among Millennials. We’re buying fewer cars, we’re taking out fewer car loans, we’re waiting longer to get a driver’s license, and fewer of us are ultimately doing so.