The work of Raj Chetty and his colleagues at the Equality of Opportunity project has spurred intense interest in the extent of economic mobility, measured by the likelihood that children born to low-income parents achieve higher economic status when they are adults. Their work shows a remarkable degree of geographic variation in intergenerational economic mobility. In many communities, the chances of measurably improving one’s economic prospects are dramatically lower than in others. The variations aren’t random: their analysis finds that intergenerational economic mobility is correlated with a number of community characteristics, such as residential segregation, income inequality, school quality, social capital, and family structure.

In theory, we believe that entrepreneurship is a key mechanism for promoting economic mobility. Entrepreneurs can create new businesses that give themselves—and their employees—the chance to improve their economic position. We already know that entrepreneurship is one of the critically important factors in stimulating metropolitan economic growth. Job growth is strongly correlated with an abundance of small firms. Across metropolitan areas, metro areas with more small firms relative to the size of their population see faster employment growth (Glaeser, Kerr, & Ponzetto, 2010).

Fast growing, entrepreneurial firms may be particularly important for providing opportunities for upward mobility because they tend to hire more younger workers than other bigger firms (Ouimet & Zarutskie, 2013). Having a large number of young, small, entrepreneurial firms may create more opportunities for young workers from all economic strata to progress through the economic spectrum.

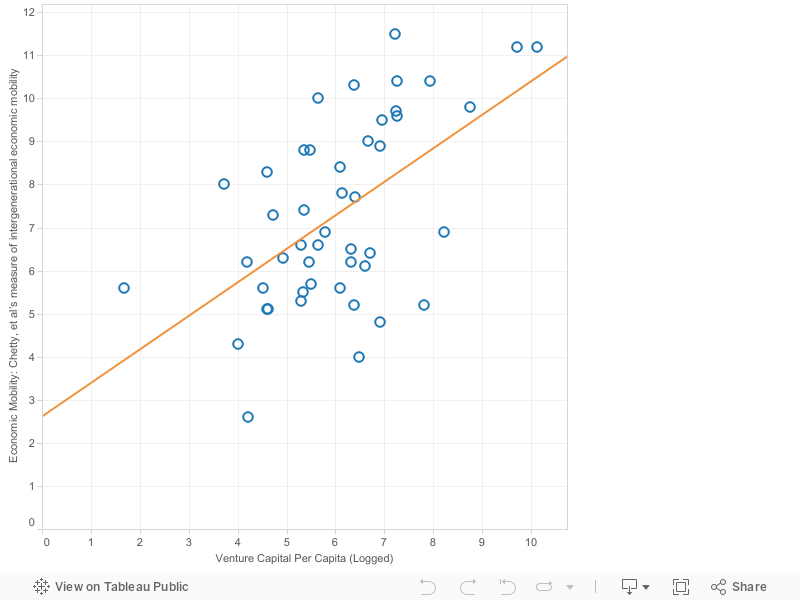

So, what is the relationship between entrepreneurial activity and economic mobility? One way we look at this is to examine venture capital per capita. (For this analysis, like most others we produce, we focus on the nation’s 51 largest metropolitan areas—those with populations larger than 1 million in 2012.)

Venture capital investments are a key indicator of entrepreneurial activity. We tabulate data from the National Venture Capital Association on the dollar value of venture capital in 2011 divided by the population of the metropolitan area. Because of the very large disparities in venture capital per capita among metropolitan, we took the log of this variable.

We compare the venture capital per capita in each metropolitan area with the level of intergenerational mobility by metropolitan area. We use Chetty, et al’s measure of intergenerational economic mobility: the probability that children born to families in the lowest income quintile had incomes as adults that put them in the highest income quintile. Among the nation’s largest metropolitan areas the probability of moving from the lowest quintile to the highest varied by a factor of about three: a four percent chance in the least economically mobile areas to a nearly 12 percent chance in the most economically mobile areas.

The chart below shows the relationship between venture capital and economic mobility for these large metropolitan areas. The data show a positive relationship between venture capital and economic mobility: cities with higher levels of venture capital have higher levels of economic mobility. (The R2 of .31 suggests that this is a statistically significant relationship.)

This strong positive relationship is not something we can immediately claim as a causal link—however, it has implications for further study. It also raises interesting questions: if cities attract more venture capital, will they be able to attract more young talent? And how will that impact economic mobility and inequality within the city?

In a future post we will examine the link between the number of small businesses in a metro and economic mobility, and conclude this segment. (To read more on economic opportunity, go here, and to read more about innovation and entrepreneurship, see our work here.)