A few months ago, we published a three–part series about why the way we measure housing affordability is all wrong. In particular, we objected to using the 30 percent ratio of housing prices to income as the benchmark of “affordable,” basically because depending on income and other necessary expenses, a given household might actually be able to spend way more than 30 percent of their money on housing—or way less.

But now we have another nit to pick. To wit, the nit: measuring housing prices by only looking at the median. Recall from math class that in any given area, the median-priced home is the one for which an equal number of homes are more and less expensive. But most of the time—San Francisco and New York and their peers in housing market dysfunction notwithstanding—we’re not mostly concerned with the median housing purchaser; rather, affordability problems will be concentrated in the lower part of the earnings scale, and so what really matters is the lower end of the home price scale.

For an illustration of this problem, imagine two neighborhoods. In both places, the median home costs $300,000. But in the first neighborhood, every home costs exactly $300,000, while in the second, there are a range of homes from $100,000 to $500,000. Although both neighborhoods have the same median home price, the second neighborhood has some homes affordable to low-income people, while the first neighborhood does not.

So rather than the median, or 50th percentile, home price, we really care about something like the 25th percentile: the home for which 75 percent of homes are more expensive.

Now, to be fair, the price of a place’s 50th percentile home strongly predicts the price of the 25th percentile home. If the median housing price hits a million dollars—as it does in, say, San Francisco—you can be quite confident that the 25th percentile home is also far, far too expensive.

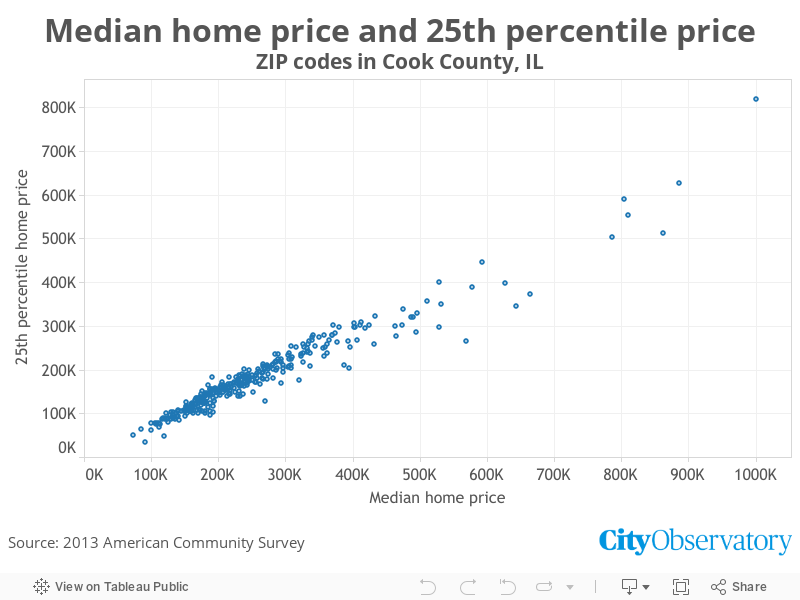

But in more normal markets, there is enough variation in 25th percentile prices in places with the same 50th percentile price to make a meaningful difference in affordability for lower-income people. Let’s take Chicago, for example. Happily, the Census has home price estimates for both the 25th and 50th percentile homes (and 75th—the home for which just a quarter of all homes are more expensive—but we’ll leave that to another post). If you plot these two prices by ZIP code in Cook County, which includes Chicago and its inner-ring suburbs, this is what you get:

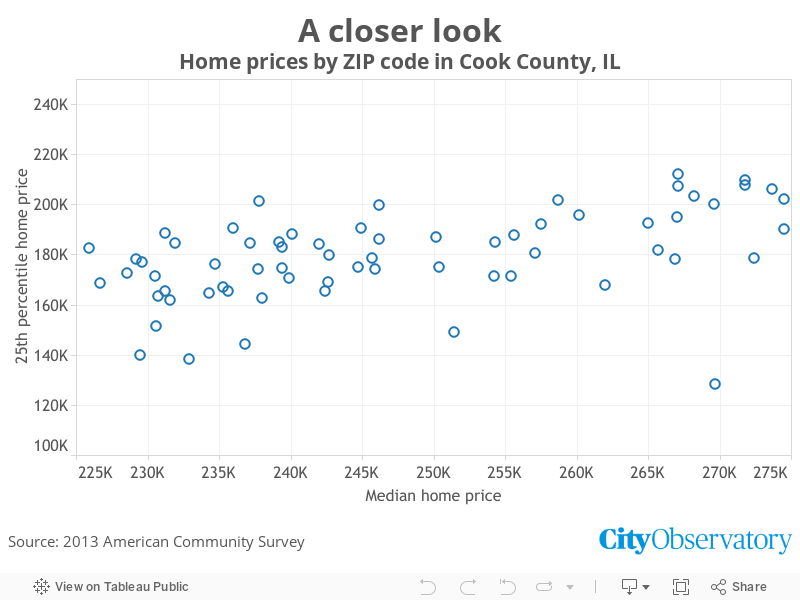

As we said, the median home price of a given ZIP code very strongly predicts its 25th percentile price. But let’s zoom in a bit—to, say, anywhere with a median price within $25,000 of $250,000.

Now we can see a strong amount of difference. Right on the $250,000 median price line, for example, ZIP code 60645 has a 25th percentile home price of about $149,000, while ZIP code 60422 has a 25th percentile home price of $187,000. In the simplest terms, then, a low-price home in 60422 is a full 25 percent more expensive than a low-price home in 60645—even though an average-price home is almost exactly the same in both places.

How does that happen? Well, zooming in on what these two ZIP codes actually look like on the ground, we can hazard a guess. ZIP code 60422 is in suburban Flossmoor, which has a small, walkable, “illegal neighborhood”-type downtown around a commuter rail station, but otherwise is almost entirely made up of single family homes, ranging from medium-sized to large.

ZIP code 60645 is in the West Ridge neighborhood of Chicago’s far North Side. It has its share of medium-to-large single family homes; but it also has a large number of multi-family buildings, from a large tower-in-a-park development to copious numbers of two-flats, three-flats, and larger lowrise apartment buildings.

The contrast is actually a brilliant illustration of one of our favorite topics, which is the way that traditional, “illegal neighborhoods” can use a diversity of buildings to create a diversity of people. West Ridge simply has many more kinds of homes than Flossmoor: there are single family houses for parents and their children who can afford a $250,000 (or more) home; there are relatively large apartment and condo units in lowrise buildings; and there are smaller apartment and condo units in lowrise and highrise buildings that provide a stock of affordable housing without subsidies.

It helps, too, that West Ridge has buildings from a variety of time periods, dating back to the early 1900s. As we’ve written before, new construction is almost never affordable to people of low or moderate incomes—but often homes that are built for the upper middle class become much more affordable after a generation or two. Much of the low-priced housing in West Ridge fits this story.

All these differences add up to very different neighborhood demographics. West Ridge has a median age, income, and poverty level that are all fairly close to those of the city of Chicago or metropolitan area averages. In Flossmoor, by contrast, the median age is 46—more than a decade older than the metro area median—in part because there are few homes suitable for young people who might not yet have a stable middle-class income. Moreover, just 2.9 percent of residents in ZIP code 60422 live below the poverty line. As we’ve covered before, while that might sound like a good thing, in a region where nearly 14 percent of people live below the poverty line, such a low level in an individual city isn’t a sign of economic success—it’s a sign that Flossmoor has (in part) used its built environment to exclude low-income people from one of the most opportunity-rich parts of Chicago’s south suburbs. Economically integrated West Ridge, by contrast, manages to keep a strong middle class while remaining inclusive of people whose incomes are much lower.

But none of these differences can be explained by median home price—because West Ridge and Flossmoor have almost identical median prices. Instead, we need to look at the price of a typical low-priced home to understand what’s going on.